Reviews of the Year are the standard filler in the run up to the Christmas Holidays, while the Year Ahead prediction industry fills the space between Christmas and New Year. However, we started the note with a quote from the famously gloomy Danish Philosopher, Soren Kierkegaard because we recognise that to look forward also requires that we look back for context and understanding.

Life can only be understood backwards, but it must be lived forwards

Soren Kierkegaard

Momentum or Mean Reversion?

Applying Occam’s Razor to most things in Financial Markets and certainly forecasting/predicting is essentially to ask 3 questions 1) ‘Will it continue moving in the current direction? Or 2) ‘Will it revert to some form of mean? In either case, 3) is it meaningful? With this framework in mind let us consider last year and this year.

Western Economies and Markets in 2023

In 2023 we saw two powerful mean reversions in markets as both components of the 60:40 portfolio first slowed downward momentum and then rebounded right back to (and past) their trend mean positions. Equities began the process in January, stalled mid year and then finished with powerful positive momentum. Bonds, by contrast, continued their 2022 negative momentum, with a sharp, final sell-off mid-year, before seeing strong mean reversal in the final quarter, helping to contribute to the Equity Rally. Unusually and importantly almost all the mean reversion and momentum in US Equities - and at 60% of Global Markets this dominates the Asset Class - came from a small number of Mega Cap tech stocks.

Elsewhere, the Nikkei appeared to start a new uptrend (maybe a long term mean reversion) while the FTSE and the Euro Stoxx 600 basically traded sideways within a +or - 5% band

Last January, our overall assessment of markets was that they were too bearish about the economy, with widespread predictions of a recession and also that they were too confident about a ‘second leg of an equity bear market’, based as it was on a combination of a) their economic view and b) a simplistic ‘this is what happened last time’ approach, neither of which we thought bore much scrutiny. Our view was that there might not be a new bull market, but that the bear market was over. We said that the economy and inflation would slow but that rates would not come down sharply. Pause not Pivot.

H1 Equity markets were largely about recovery and mean reversion in the Mag 7, rationalised to be about AI - with a Bank panic thrown in the middle

We were right that there was no recession, nor a bear market, that inflation would slow and that rates would not come down sharply, but from an investment viewpoint did that actually matter? In some senses not really, for the only thing that delivered meaningful equity returns in 2023 was the ‘bet’ on the Magnificent 7 mega cap tech stocks, which brought the video game style investing of the ‘meme stock’ world into the mainstream. Initially a recovery from an oversold position, the momentum effect as the big momentum ETFs recalibrated mid year to sell energy and buy tech (something we discussed here) was ‘explained’ by the excitement about AI mid year.

Meanwhile, as Silicon Valey Bank and others revealed themselves to be more like badly run bond funds with no understanding of Duration risk, the markets had a Mad March Moment and the short term traders and some asset allocators panicked about another Lehman, offering long term investors the opportunity to buy some quality stocks at decent prices.

However, by H2, momentum was driving markets and asset allocators scrambled to buy the NASDAQ over the S&P500 ( a more common allocator trade than the equal weighted versus market cap weighted S&P used by wealth managers), as being underweight something that is going up is a powerful motivator to self preservation.

Q3 and the end of Japanese Yield Curve Control triggered the final selloff in the Western Bond Markets, taking equities with them

Just as equites other than the recovering M7 began to stabilise and rally at the end of Q2, the Japanese Bond market spoiled the party. After decades of ultra low interest rates, the Japanese central bank, under its new head Kazuo Ueda finally moved to tighten monetary policy in the summer, moving to the equivalent of a managed float in terms of setting rates for the 10 year JGB, which immediately shot up in yield, triggering all manner of market mechanics as years, if not decades, of financial structures had to unwind. The ultimate mean reversion. US Treasuries leapt to 5% yield and all the indicators for our model portfolios jumped to red at the end of Q3. Western focused analysts (as always) explained this in terms of expectations about the Fed and US inflation as well as concerns about the new conflict in the Middle East (although this came after the move in yields).

Bond Math(s) was key to Q4 as fundamental investors finally came out of cash

However, as we argued in late October, the speed and extent of the sell off in Western Bond markets was such that when US 10 year yields hit 5%, there was a great (and rare) opportunity for long-term investors, presented by the Asymmetric Bond Math(s); a 50bp increase in yields at that point offered a flat return to long bonds over the following 12 months while a 50bp drop offered a double digit return. Long term investors started to move and, as yields tumbled, others, hiding at the short end of the curve and knowing they were taking re-investment risk in matching assets and liabilities, also rushed to extend duration. This pushed yields back to 4.5% and then beyond, briefly going below 4% by end year.

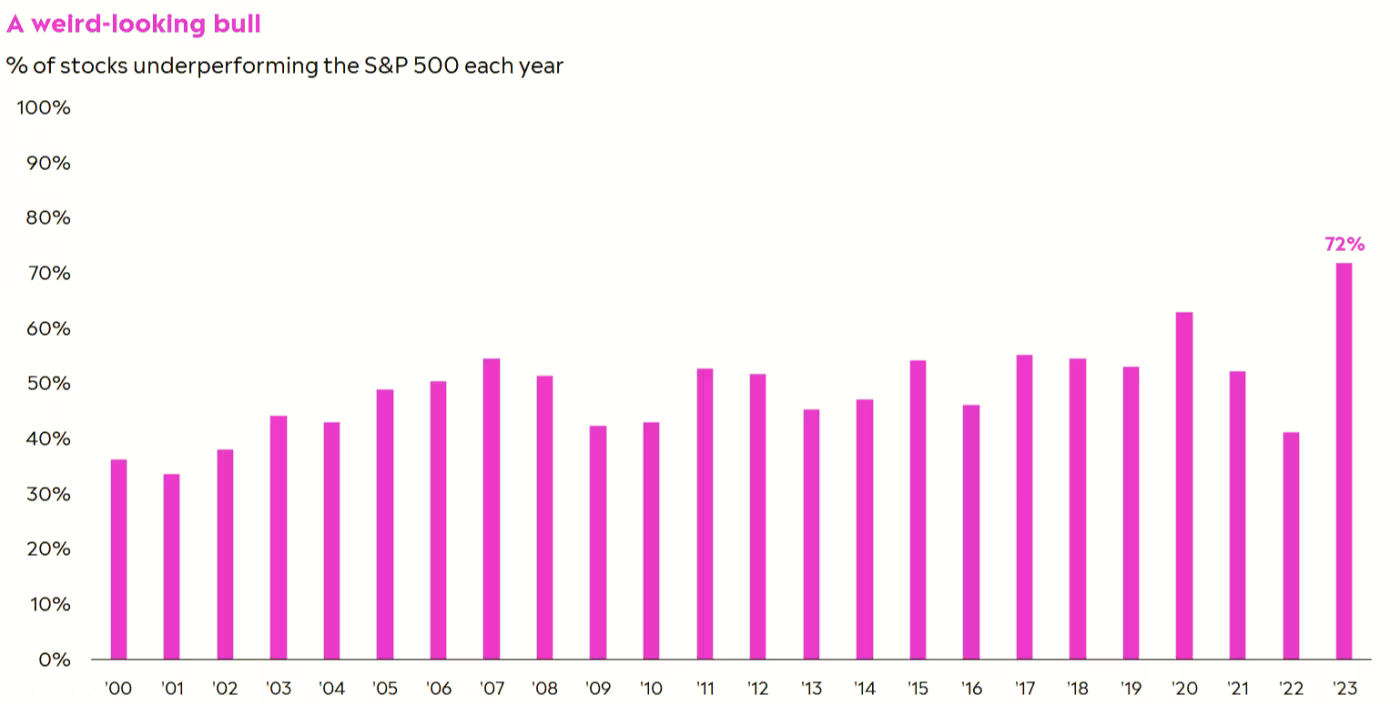

This sudden de-risking of bond markets fed through to equities and with huge short covering they not only stabilised but delivered a powerful year end rally, producing some very attractive benchmark returns. However, as noted, the nature of the underlying returns was very strange. We found that during 2023, the Magnificent 7 and a few associated stocks went from expensive in 2022 to good value at the start of the year and then back again, while an ‘unprecedented’ 72% of stocks underperformed the benchmark in 2023 - as highlighted by Etoro strategist Callie Cox in the Financial Times with the following chart.

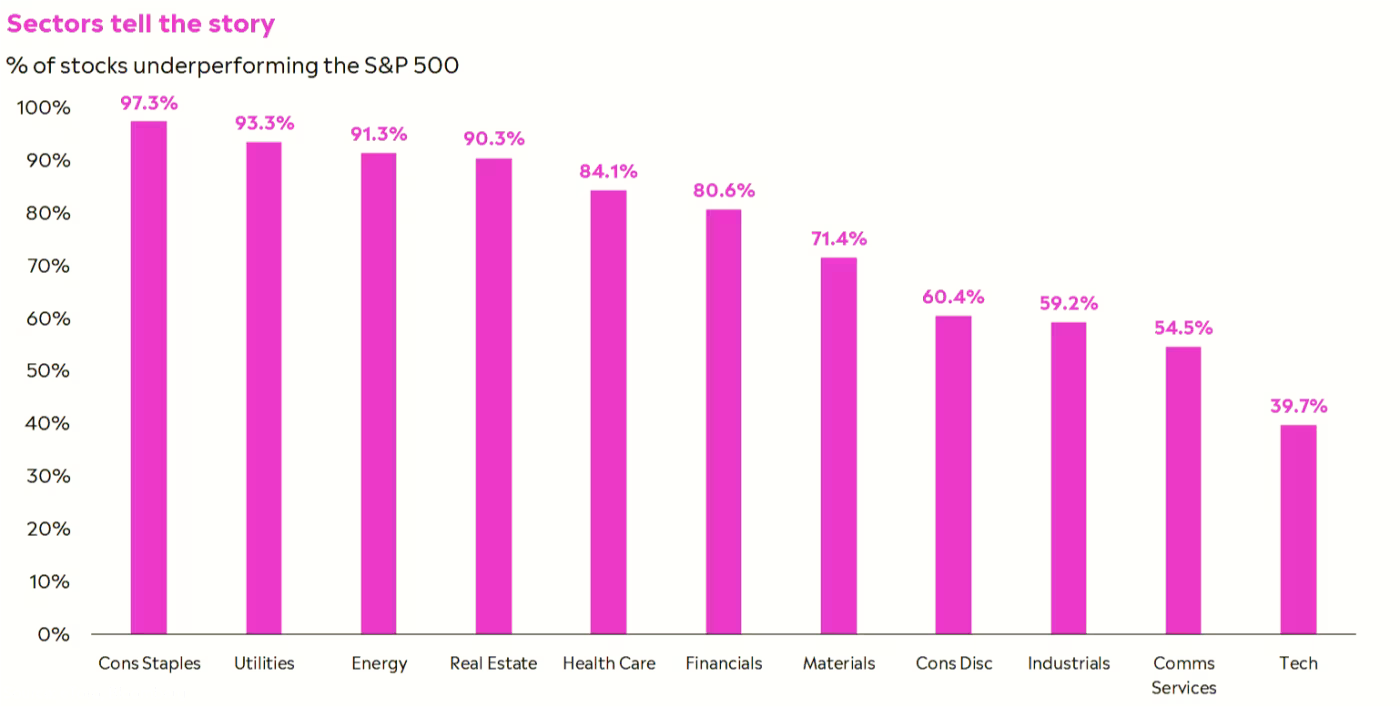

They also included a second chart that we think sums up the US Equity markets in 2023 very well, the % of each sector that under-performed the S&P500 benchmark - highlighting the huge distortion produced by the tech ‘bounce’/mean reversion.

Market Mechanics as well as fundamentals drove sector relative returns

In effect, investors were punished for diversification

Many, sectors, were basically flat on the year, with only a dozen or so of the 40 stocks in the XLP ETF Consumer Staples Sector for example recording a positive return at all, although this was probably due to the fact that they had held up well in the big down year of 2022. The similarly flat, but relative underperformance, of both energy and materials meanwhile was less to do with the global economy - although it was spun as such by the bearish economists - than the fact that they were relatively strong in 2022 (mean reversion) and the other side of the H2 momentum ETF trade that gave the second leg up to the tech stocks. As such, they were cheap, high yielding cyclical value sectors that under-performed - despite the consensus being wrong on the economy.

By contrast, Utilities, Real Estate and Financials were all seen, understandably, as ‘losers’ under a higher interest rate regime, although as we noted on a number of occasions - including when Silicon Valley Bank blew itself up back in March - the situation in Europe (Credit Suisse aside) is generally very different - which is why, in contrast to the US, European Financials were some of the better performers in 2023.

The Rest in 2023

China began the year with some strong mean reversion, before seeing that all unwind as sentiment and narrative were firmly negative in the second half. Hong Kong is very similar. India, by contrast seems to be benefiting from a positive narrative and is in a positive momentum phase. Looking at Emerging Markets ex China, as we are now doing, showed an emerging positive momentum here too.

The concept of The West versus the Rest was something we talked about a lot in 2023 as Geo-Politics drove a lot of underlying trends. Much attention was paid to De-dollarisation, which was largely mis-represented as an end to the $ status as a Reserve Currency, which is not happening, instead of a reduction in the use of the $ as a currency for third party transactions, which definitely is in the context of the BRICS.

Euro the big loser so far in de-dollarisation

However, one big and largely overlooked story of 2023, which has interesting implications for 2024 and on, is that the use of the Euro has collapsed; according to Statista, the use of the Euro in SWIFT transactions during 2023 fell from 33% in January 2023 to 13% by the end of the year, with the $ jumping from 45% to 60%. This is almost certainly linked to the ban on SWIFT in Russia following the Ukraine invasion and also the subsequent sanctions leading to the shift to Europe buying LNG from the US and Qatar in dollars. In effect, as the BRICS+ start to use fewer dollars, Europe is being forced to use more dollars and fewer Euros.

Asset Allocators ‘dis-invested’ China for (career) risk reasons

At the start of 2023 we noted that the year-ahead notes were largely ignoring China as it came out of a Covid induced Coma and saw this as an opportunity for mis-priced growth. The traders jumped on the idea mid way through the first quarter, but it didn’t last beyond mid year and as we subsequently discovered, not only did the Asset Allocators not follow through with buying, they actively sold, creating the conditions for a bear market in Chinese Equities. Much of the motivation behind this selling was risk, or to be more precise, job preservation risk. Having been left stranded in Russian assets post Ukraine and/or caught out by the collapse of the China ADR market in 2021, the fiduciaries at the large Institutions like Pension Funds and Insurance Companies took note of strong ‘guidance’ from the US government that ‘China is uninvestable’ and sold accordingly. As Keynes once noted ‘it is better (safer) to fail conventionally’, so missing out on a rally along with everyone else has low cost, whereas being long a market sell-off/collapse when everyone else has sold is an unacceptable career risk.

The need to justify this selling in ‘fundamental terms’ led to much of the year being dominated by the ‘China glass is half empty’ side of the debate, albeit happily encouraged by US politicians wanting to promote the US model as superior to the Chinese one at a time when ‘The Rest’ under BRICS+ were moving in the opposite direction.

While buying India and Japan for equal and opposite reasons

The net result of international investors selling China was a switch to Japan and India as ‘allies not enemies’ and accordingly the narrative was spun positively in both markets. Although we might include Japan geo-politically as ‘The West’, it is also geographically caught up with EM and ‘The Rest’. We have liked the Warren Buffet trade on Japanese wholesale and trading companies for some time - essentially a carry trade on their relatively high yields and an operational leverage trade on the global economy and trade - but remain somewhat sceptical on the ‘Japanese renaissance’ theme. Many of the companies we like thematically in areas like Robotics and Automation are in Japan however, so we can definitely see reasons to look here. The only note we would add is that a large part of the return in Yen in the second half was a currency play - the underlying market traded largely sideways. India meanwhile has certainly done well as a middle man thanks to the Russia sanctions and has definitely benefitted from some powerful positive narrative as (once again) ‘The New China’. In fact it is perhaps better thought of as the New Anti China.

The West in 2024

We see fading positive momentum from Q4 as a background for Q1 2024, both in Bonds and Equities, even as the narrative is spun positively by politicians seeking re-election. Cash has gone from the one asset that will not give you a capital loss, to the one that won’t give you a capital gain and will likely act as a stabiliser at the bottom of smaller mean reversal bands. Positive underlying cash flows will keep a modest upward trend to most equity markets and while moderating inflation will allow central banks to ease a little, we think bond markets will struggle to be too inverted

The economic consensus is now rather confused, not least because the rally in the bond markets has one group of economists wanting to buy bonds and sell equities because of a recession and a separate group wanting to buy bonds and also buy equities because there is no inflation and we are back to Goldilocks and a soft landing.

Generally we would note that most City Economists are employed by the Fixed Income Departments and are thus always gloomy as a ‘reason’ to always buy bonds, but we would also throw another variable in here; the US Election, where the set is being dressed for a ‘US Economy is Great, Vote Democrat’ narrative, that is already being actively embraced by the (heavily Dem leaning) US Media.

We would be somewhere in the middle; we believe that just as the Monetary Easing put in place in 2020 led to inflation in late 2021/early 2022, so the tightening that followed will show up in slower activity this year, but that having seen peak inflation and peak rates, consumer confidence may now pick up, particularly in areas like housing. However, while rates may be easing, they are not coming down to pre-covid levels and businesses that ‘need’ this to happen will continue to struggle.

Equally, after the Santa Claus rally, the consensus now seems to be that there is a new Bull Market in stocks that was born in 2023. We remain of the view that the end of a bear is not the same as the start of a bull, certainly not when the market was as narrow as it has been. Moreover, the buzz word of 2023 that was AI is going to offer both opportunities and threats in 2024 - and that includes the Magnificent 7. Buying the ‘picks and shovels’ of a new theme is fine for the first round, but new winners will emerge (most of the Magnificent 7 were the second order winners from the internet after all). We suspect that combining AI with Robotics (rather than just chat) will be a big emerging theme, which is why we still like Robotics and automation stocks.

When we called the long bond as one of the trades of 2024 (with the general Caveat that this is not investment advice), we also said that the market would not hang around and it certainly hasn’t. We also added that our adjusted Taylor Rule suggested 75bp of cuts were credible - which is now pretty much consensus thanks to the Fed’s latest statement and with 10 Year yields down from 5% to 4% the asymmetry that made it such an attractive trade has now gone. The biggest challenge for Bonds this year will now be cash, as a moderately inverted yield curve continues to hold a lot of bond cash at the short end. The Pause not Pivot call of last year is a Modest Ease not Pivot call for this year. Interest rates are mean reverting, but only to a 2-3% inflation environment, not a 0-2% one. Ultimately that means cash can come towards 3%, but not this year.

The Challenge of (and for) cash

The challenge for Asset Allocators is that, while in 2023 it was seen as attractive, being the one thing that wouldn’t give you a capital loss, in 2024 cash will be the one thing that won’t give you a capital gain. Cash will, correctly, be the hurdle rate and will not return to levels that will make highly leveraged and complex trades very profitable again, but as it slowly returns to equilibrium (we would say around nominal GDP), focus will be on how companies can earn a real yield and thus on attractive cash flows and unleveraged, Quality, balance sheets. On this basis the unloved stocks like US Consumer staples, with a yield of 3% and a P/E of 20, may start to get some attention. Similarly, European and Japanese ‘quality’ stocks with strong balance sheets and good dividends may become rather more attractive to international investors looking for the Three D’s ‘Diversification, Disciplined Investing and Dividends.

The Rest in 2024

A mean reversion in China/Hong Kong remains the bold Mean Reversion call for 2024, but is one that will emerge only as and when the negative momentum fades. Positive momentum in India is at risk however, on account of valuation and the upcoming Elections, suggesting a broader EM ex China as the best combination of value and momentum. Japan positive momentum has stalled, but we see value and mean reversion in the Yen as the most likely catalyst for renewed positive momentum in 2024.

As part of the ‘US Never Had it so Good’ campaign, there is obviously the equal and opposite ‘look how badly our enemies are doing’ narrative, like the headline on this piece from CNN, saying “China’s economy had a miserable year. 2024 might be even worse”. Despite the fact that the article itself actually acknowledges that China is still expected to grow by 5%, about 10x the speed of Europe, and even if the tensions of Taiwan ease dramatically in the next few weeks after the Election, the bipartisan nature of China-bashing in a US Election year means that any stabilisation in China markets will have to come from elsewhere; the international investors in the US are staying away.

Comparing the 2023 US and China GDP growth in nominal US$ terms has also become quite widespread practice, even though this is down to a) higher US inflation and b) a higher US $, neither of which are good for US corporates facing competition from China. This is important when considering US international earnings in 2024 - as well as positive earnings from ‘The Rest’. Naturally there is a lot about ‘the Property Crisis’, ignoring the deliberate nature of its implosion and the fact that the main losers are not Chinese households (as claimed) but the Western investors in the equity and offshore debt of the property developers.

The other cut and paste meme on China has been ‘soaring Youth Unemployment’ but even this piece from the BBC acknowledges in the body of the report that the widely touted ‘problem’ with 21% youth unemployment in urban areas actually only represents 1.4% of the available workforce. At the same time China’s shrinking workforce due to demographics is presented as a problem, while Japan’s is not. India’s growing population is cited as a good thing but the fact that its youth unemployment is not only higher than China’s but that the size of the youth population relative to the overall workforce is almost 40% is disregarded.

This is not to indulge in ‘whataboutism’, rather to point out that the preference for Indian and Japanese markets is at least partly influenced by this presentation of the macro, which in turn is influenced by Geo-Politics. We find that such cognitive dissonance does not tend to last very long in markets.

Conclusion

Macro views often follow the markets rather than lead them

The Macro was too bearish in early 2023, influenced by the poor performance of markets in 2022, and subsequent events supported our own view of slowing growth and inflation, but no recession and no second leg to a bear market. Nor any great easing of interest rates. From a macro viewpoint, we are relatively unchanged, but the strong rally in both bonds and equities in Q4 has left some (a lot) of Macro now as overly positive in early 2024 as they were overly negative in early 2023.

In 2022 the call was to be out of the Magnificent 7, just as the call for 2023 was to be in it - although few active managers did both. This year, there is no pressing case for either, but instead a renewed case for Diversification - both within the US and internationally - as well as dividends and disciplined investing (rather than chasing memes and believing too much in narratives). Initially we suspect some small mean reversions as momentum fades - both positively and negatively - with (excess) cash providing underlying support at the bottom of trading ranges. Politics will be important, but from an investors’ point of view, outside of narrative management it will be the extent to which monopolies and ‘moats’ are challenged by populist politicians - shifting risk profiles.