At the end of September we started to see some unusual behaviours in markets generally, but particularly in the bond markets. This was notionally pinned on the Fed announcing ‘higher for longer’, but, as we noted in the October Market Thinking, this felt like an ex-post rationalisation to us. Similarly with the discussions about real yields and changing expectations about economic growth. More likely we felt was that, as is almost always the case, there are not only weak hands needing to sell to strong hands (see post), but that the weak hands are actually forced to do so by some, usually regulatory or rules based, catalyst.

Our favoured culprits remain Japanese institutions being forced to fill holes in their balance sheets as the Japanese bond market sold off with the ‘beginning of the end’ of Yield Curve Control in late June. The fact that US Treasuries and Gold were both still positive in Yen terms and that they were both suddenly weak at the end of September suggested to us that there was some Q3 balance sheet management going on. This is very similar to the issues faced by Silicon Valley Bank in March and the UK Pension Industry in September 2022, rules and regulations are forcing something akin to a margin call onto large financial institutions making them both price takers and price indifferent. They are not selling because they want to, nor are they selling what they want to. They are selling what what they can.

Institutions who were 'regulated in' to buying bonds are being 'regulated out'

This goes to the heart of the new New Normal. Post 2008 an increasingly large part of the demand for ‘risk free’ assets was met by financial institutions being driven by Rules and Regulations that ‘encouraged’ them to switch from ‘risky’ equities to fixed income products, which was naturally extremely helpful for those, including governments, who had so many risk free products to sell them. This led to the Alice in Wonderland world where bonds were being bought for capital gain and equities for yield and nobody thought paying 237 for a 100 year Austrian bond yielding 0.4% and guaranteeing you a 58% loss if you held to redemption was a bad idea. “Not my fault, regulator and risk model made me do it”.

And now that is reversing, the same rules that said Austrian bonds were a low risk strategy with a 0.4% yield and a guaranteed loss of 58% are now saying that buying now with a yield of 3.45% and a guaranteed gain of 60% is a high risk strategy. Our central investment philosophy is based in Behavioural Finance, the idea that market participants do not act rationally, at least in the short and medium term and that they ‘make mistakes’ like selling at the bottom and buying at the top, running losers and cutting winners, have recency bias, display herd behaviour, are subject to anchoring and so on. But this is somewhat different, this is not emotional investing, indeed it is the opposite. What we are seeing is an equal and opposite application of the Rules based Error of the new Normal, the bear market Yin to the Bull market Yang. Selling is being done by ‘custodians’ rather than investors, who are merely following the ‘rules’. As such, we are wasting our time trying to anticipate what will change their opinion, because nothing will. Only the rules.

How far does it go?

Nevertheless, and true to form, the economics profession is coming up with its own economics based explanations as to why Bond Markets have sold off with targets for Fed funds rates based, as ever, on some variation of something known as the Taylor Rule - i.e. a simplified model of where rates should be on the basis of all the things economists care about, such as the economic notion of output gaps and spare capacity in the economy that drives inflation and output. As such this drives the focus on all the high frequency data like Non farm payrolls. This ‘Rule’ is, of course a very different type of rule to the ones that are forcing fixed income investors to buy or sell regardless of fundamentals. In particular, it seems to be a rule that the Fed don’t actually follow.

Where rates should be on the basis of a model and where they actually will be are very different

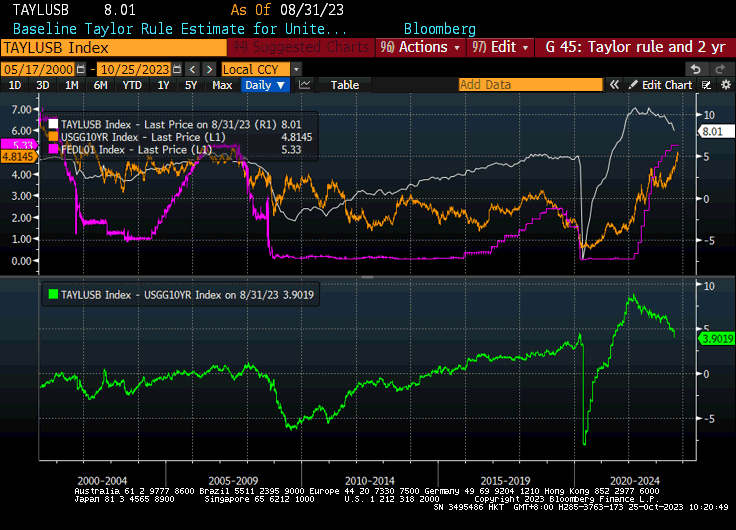

Consider the composite chart below that we have put together from Bloomberg . The top panel shows the Bloomberg Baseline calculation for the Taylor Rule (which is as good as any) compared to both the 10 year bond and the Fed Funds rate, while the lower panel displays the spread between the Taylor Rule ‘price’ and the 10 Year Bond yield.

Baseline Taylor Rule a better predictor of the 10 yr than the Fed

At first glance it says that rates should be ‘even higher’ - the white line - and for most of the economists still in the bond bear camp this is the key. For them, this means there is further to go. However, as always, your output depends on your assumptions, and in this case the key to their assumptions are what they assume about the Fed’s assumptions.

On this basis further reflection shows that the model has been ‘wrong’ for over a decade, indeed from the period straight after the Financial Crisis, which suggests that the Fed has been ignoring the economic rules. More interesting is that while it has never been very accurate for Fed funds, up until the Global Financial Crisis, the Taylor Rule was actually a pretty reasonable proxy for the 10 year bond, even if it was ‘useless’ for predicting Fed Funds rates.

In our view there is a good reason for this, which is that embedded in the Taylor Rule calculation is an assumption about Target Real Rates. The default on the Bloomberg is 2%, but conceptually, why should Fed Funds offer any real yield at all? A target of zero real return would be more consistent, allowing for term and risk premium for bonds. Equally, if Bond markets are indeed concerned about the economics, then they would ‘set’ a real yield more consistent with the Taylor Rule. In other words, we would only expect the Taylor Rule to ‘work’ with a flat yield curve, ie where no term premium and/or real yield is required.

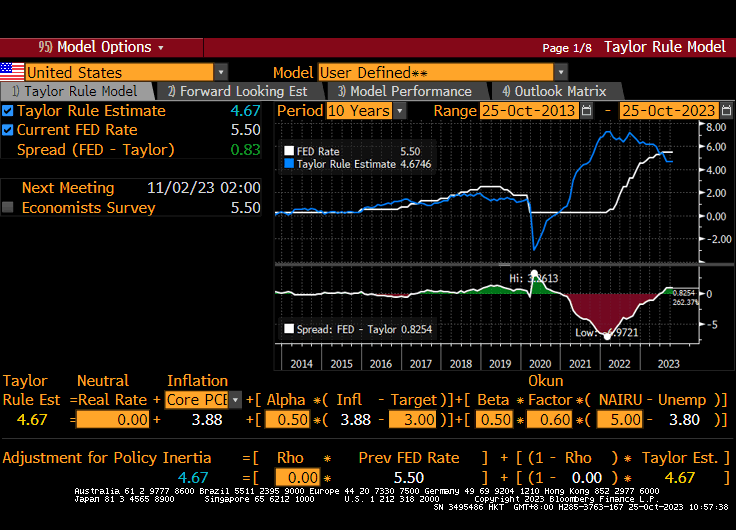

As an experiment, we created our own ‘Taylor Rule’ to model Fed Funds, using Bloomberg’s model, but with a few different assumptions, specifically on real rates, (but also on the Okun Factor and the NAIRU for those that care) and we got the following.

Targeting zero real rates a better ‘fit’ for the Fed, but also now suggests a possible 75bp lower

Here we see a much better ‘fit’ for the Taylor Rule and indeed, if we had put in a target rate for inflation of 2% - which was after all the official target - then it would have been within +or- 50-100bp over much of the last 10 years (Covid madness aside). Now, to be clear, we are not saying that is where Fed Funds rates will go, rather that the bond bear models of ‘cyclical growth’ saying rates need to go even higher and which are based on this interpretation of Fed think are actually over-riding their own internal logic. If the Fed is indeed following the Taylor Rule, then this ‘better fit’ model suggests that, if the Fed maintain a 2% inflation target, it would have a rate very close to where we are now. However, if they are happy to accept a structural shift in inflation to target 3% - ie in the middle of a 2-4% band and as we have in our ‘model’ , then up to 75bp could be justified right now, even without any slowdown.

So what does this mean for Bonds?

It’s about Duration and the Curve

Our argument is that the Fed are holding rates higher than the Rule would suggest, just as they held them lower, but that the likely normalisation may be around 50-75bp down at the short end, even with no weakening of the economic data. If, we return from the abstract world of Economic modelling, Fed Fund watching and where things ‘should be’ to one where we no longer have the Alice in Wonderland Rules of ‘risk management’ (ie no forced buying or selling) and look where we think bond yields might probably be, we can look at the following table.

We can see how the Bond Math - as they say - is now asymmetric, a 50bp rise in yields offers less downside than a 50bp fall offers upside over the next 12 months thanks to the combination of high current yields and duration effects. This is important for bond managers, most of whom we should not forget are in a ‘walled garden’ of fixed income. They are not making decisions over which asset class to buy, or which geography to buy, they are almost entirely concerned with where they sit ‘on the curve’.

The Fed are sellers not buyers and are playing chicken with the government who are also sellers. The end game is to slow budgets and get US$ cash out along the curve

For the last 24 months fixed income managers have been steadily moving shorter and shorter and many are now also holding T-bills, in most cases via the Money Market Funds, whose assets have ballooned to something around $6trn. The key is when does this ‘wall of money’ (copywrite Japan 1988) start to move? The obvious trigger would be when the Fed ‘blink’, but here we would caution that our take (for what it is worth) on this is that the Fed is not looking at the Taylor Rule so much as at the Federal Government. They ‘know’ that it was their monetising the Federal Government’s Covid spending that triggered inflation, which is why they are draining liquidity as quickly as they can. This means that, along with the rules based selling by institutions, they are also a relatively price insensitive seller of their bonds at the same time as the Government keep issuing more. As such, this would imply that the next move will be a small cut - possibly in line with our adapted Taylor Rule, perhaps as a one and done and not a ‘pivot’. This would cause a flood into the longer dated Treasuries and re-stabilise things, allowing the Fed to use it as a stick, much as the BoE did to influence politicians in the Election year.

Everyone’s a seller. Until they stop

Thus, with the usual caveat that this is not offering investment advice and is for information purposes only (do your own research and always speak to an adviser) we would have to agree with a slowly emerging consensus that this duration switch is probably one of the top trades for 2024 and that putting it on now also makes a lot of sense, as long as your clients understand you are not trying to call the bottom. This is not a trade, it’s an allocation shift. We can’t say if the rules based distressed selling is over, or that the Fed will signal that their tightening is over between now and Thanksgiving, but we are pretty sure that if either of those things happen, markets won’t hang around for a second chance.