The latest CPI numbers from the US have produced a flurry of activity in ‘noise markets’ as leveraged traders in Bonds, FX and Commodities scramble to reverse positions and invert the narrative around inflation and interest rates. Hopefully, this will now prevent the overtightening ‘required’ by the computer models that are fixated on interest rates controlling inflation through demand, ignoring the impact they have on supply as well as the role of monetary expansion. Policy error remains one of the biggest threats to economies and markets, so with a bit of luck, this timely intrusion of reality into the world of computer models may well save us from central banks repeating their mistakes.

This week’s latest CPI ‘print’ from the US produced an immediate reaction from the excitable folk in the fixed income and FX markets as they switched from chasing the notion of the Taylor Rule (the theory that strong employment means inflation and thus higher rates) to chasing headline inflation itself. In doing this, they are simply mimicking what they see as the policy process of the Fed - running fancy computer models of the output gap on the one hand, while in reality simply reacting to the last high frequency data point on inflation.

Thus, as we said in the latest monthly, with long term investors having come in and bought long bond yields at just over 4% last week, they find themselves back at 3.75% a week later - a nice turnaround of 3% - which is a big deal in fixed income - especially if you are a leveraged trader. Technically this is likely to harden 4% as a yield support level for bonds now, while fundamentally, as CPI drops from 5% to 4% and now 3% in the US, that 4% offers a real yield to be ‘locked in’.

A 3% rally in bonds in a single week is a big move for a leveraged fixed income trader, but a 3% drop in the Dollar is an enormous move in the even more highly leveraged world of FX

Meanwhile, in FX, the flip flop from tighten to pivot to tighten and now, likely, pause has seen the $ ‘collapse’ by over 3% on the trade weighted index, (which is an enormous move for an even more heavily leveraged FX trader) dropping below 100 for the first time since April 2022 and will likely have traders looking at a fibonnaci retracement of the strength since June 2021, targeting first 98 and then 89 on the DXY.

Of course, nobody actually trades the DXY, but if we look at the major components, we see the Euro has completed an exact 61.8% retracement of its post June 2021 weakness, while sterling has been even stronger and has also broken up through the psychological 1.30 barrier. The Yen meanwhile, which followed a different path last year, has retreated (effectively rallied) from 145 to take support at its long term moving average of 138. This had previously been overhead resistance until what looked like some ‘funding’ trades in May and June caused it to weaken.

To the third set of leveraged noise traders in commodity markets then and we see Oil has rallied from its recent support level around $67, towards the top of its trade range at around $80. Copper, which similarly tends to trade inversely with the $ is heading back to $400 and Gold is trying to reach for $2000 again.

Cascading further down, we see the JP Morgan Emerging Market bonds ETF, seen as another inverse $ play moving higher, while the Emerging market consumers, Global Energy and Mining stocks also rallied. All on the back of a CPI print!

Risk of Policy Error receding?

We have long felt that the biggest risk to economies and markets has been policy error, and in particular the impact of the so called Triple Zeros - centralised policy around Zero Covid, Zero Carbon and of course Zero Interest Rates, all based on complex computer models which not only fail to match up to real world outcomes, but also produce unintended real world consequences that are studiously ignored by policy makers, but yet need to be dealt with by markets.

In the context of Zero Interest Rates policy, we had the unintended consequence that a near zero cost of capital produced a much bigger stimulus to supply than in did to consumer borrowing, as well as a misallocation of capital that kept zombie companies operating and allowed startups to sell below the actual marginal cost of production. Meanwhile, in savings based economies like Japan, we had decades of evidence (studiously ignored) that lower returns on savings led to increased saving, not increased spending. Both features (lower demand and higher supply) conspired to produce dis-inflation rather than inflation and yet the policy makers kept applying the same (failed) policies - looking only at headline inflation.

We thus doubt that the abandoning of Zero Interest Rate Policy had anything to do with a recognition that trying to create inflation through stimulating demand via ever lower interest rates does not actually work, but rather that, having actually created inflation through flooding the economy with liquidity during Zero Covid, they are now trying to stop that inflation by collapsing demand through ever higher interest rates(!) Same policy error, just different direction.

Low rates didn’t cause inflation - the zero covid policies of collapsing supply chains while flooding the real economy with liquidity did that - and high rates won’t cure it.

Indeed, the bigger issue is that the unintended and overlooked (by the central banks at least) consequences of low rates now reverse sharply.

Previous unintended consequences reversing - new ones arriving

Both the speed and the size of the rate of change in short term interest rates is already having a new wave of (again presumably unintended) consequences. The first of these is that the excess supply arising from low rates that caused the (overlooked) dis-inflation now goes away, leaving structural inflation some 200bp higher - ie a range of 2-4%, rather than 0-2%. Equally, in places like Japan, where zero interest rates suppressed demand, that is now rising - entirely consistent with experience and yet in contrast to the computer models. Meanwhile, lower supply and less dis-inflation is actually good for many companies’ profits as it shifts pricing power, which is one reason why corporate profits are surprising on the upside. Market are busy adjusting to this new New Normal, even if policy makers aren’t there yet.

The second, entirely predictable - and presumably unintended - consequence of a decade of Zero interest rates was of course widespread speculation and a huge asset price bubble. The fascinating book The Price of Time by Edward Chancellor brilliantly describes how this always happens when the cost of money is set below its natural rate. It really ought to be compulsory reading for central bankers and policy makers, who continue to confirm George Santayana’s comment that “ Those who refuse to learn from history are Doomed to repeat it.”

After a decade of inversion under QE, assets are reverting to their ‘normal’ roles; Bonds for income, Cash for risk management and Equities for growth and real returns.

The flip in rates is already starting to flip those previous unintended consequences and burst many of the asset bubbles - indeed 2022 was exactly that as far as bond markets went and to a large extent equities too as discount rates reversed to normal. By contrast, the process of unwinding leverage across less liquid assets such as Property and alternatives such as Private Equity, Leveraged Loans and Private Credit is underway, albeit less visible, but has yet to fully play out. It nevertheless means that assets are now reverting back to their primary purpose - Fixed Income (and some equity) for Income and Equity for growth and real returns. Cash, which in the near term is having an unintended consequence of crowding out liquidity elsewhere, is set to revert to zero % real rather than zero % nominal and resume its role as a risk management tool. Alternatives, at least those who relied on illiquidity and leverage as sources of return, are likely to return more to the ‘satellite’ part of portfolios.

It’s even more important for ‘the rest of the west’

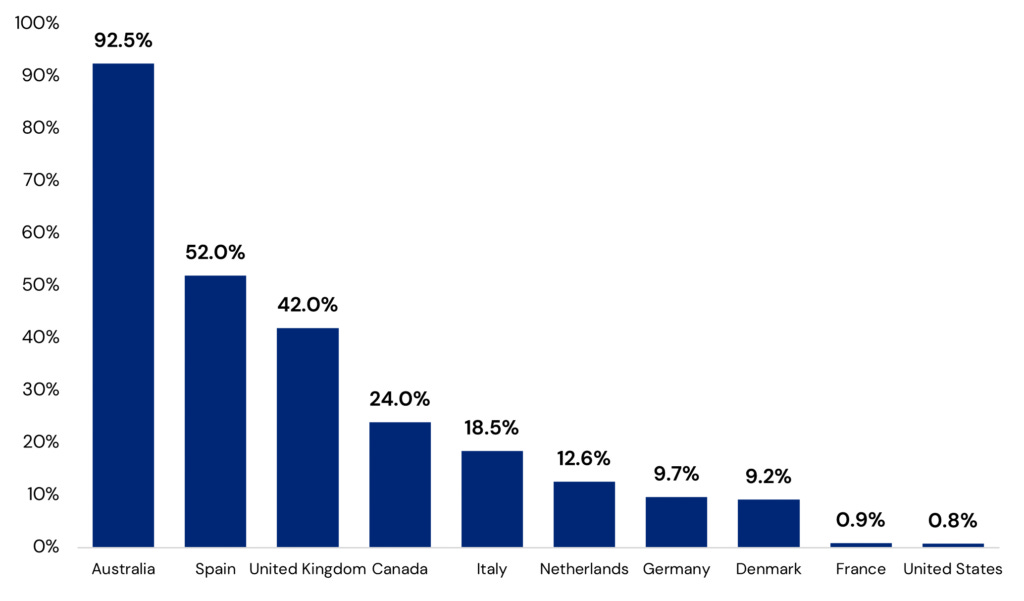

However from an economic perspective the biggest impact for many will be the housing market, where the asset price bubble was the largest and now the hike in rates will have the biggest impact. The chart below highlights which countries are most vulnerable to this Central Bank inversion - and thus by extension those who have most to gain from the Fed pausing its anti inflation campaign. Essentially it is ‘the rest of the west’, led by Australia, the UK and Canada.

In the old days, when people paid attention to Monetary variables, interest rates were said to act with long and variable lags, but, egged on by hyper-active traders, central bankers appear to have forgotten this. Moreover, the nature of household balance sheets is crucial; common sense says that if you tighten policy in a fixed rate environment it won’t have the same impact as in a floating rate environment and that higher rates for a household with a large floating rate mortgage will have a bigger impact than on a smaller, fixed rate mortgage. In effect, the impact of interest rates policy depends on the nature of balance sheets. And yet, we are pretty sure that all the central banks have similar models, assuming similar effects.

In recent years, a number of countries with floating rate mortgages have adopted a quasi fixed system, not like the US system where rates are fixed and re-financeable downwards - which gives the best of both worlds to the household - but a form of short term fix. The problem with this of course is that hiking rates when mortgages are fixed has little impact, until the fix comes off, when there is serious sticker shock.

Monetary policy is like pulling a brick across a rough surface on a piece of elastic - nothing happens for a long time and then suddenly the friction is overcome and the brick flies up and hits you in the face.

As the chart from fitch illustrates many ‘fixed rates’ are relatively short duration and are soon rolling off, such that raising rates now will have little or no effect, other than to magnify the ‘sticker shock’ when those rates do eventually roll off. The leading example of upcoming expiration sticker shock is Australia, where 92.5% of rates are set to expire or reset within 24 months, followed by the UK 42% and Canada at 24%. Spain, where 52% of mortgages are resetting or expiring within the next 24 months, or Italy at 18.5% of course has their rates set by the ECB, which is more focussed on Germany (9.7%) and France 0.9%.

Share of residential mortgages originated with rates that expire or reset within 24 months

If you are going to follow the Fed, even though it makes no sense, you have to hope the Fed stop hiking

The US, which is essentially driving ‘western’ monetary policy is barely visible at less than 1%. The conclusion is that, on the basis that these so called ‘independent’ central banks are all simply following the Fed without considering the upcoming sticker shock (that will not affect the US housing market), we have to hope that the Fed will start chasing the CPI down - or at least stop hiking. As we saw with zero Covid at least, at some point reality will kick in to counter the computer models and save us from the ‘experts’.