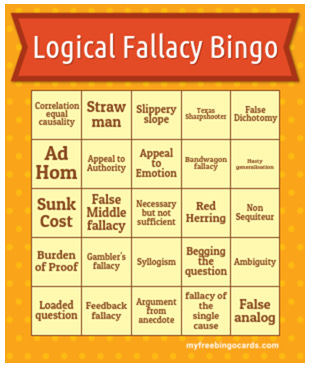

Logical Fallacy Bingo

As part of our toolkit in understanding the behaviour of Ben Graham’s Mr Market, we spend a lot of time with our logical fallacy Bingo card, not least because almost all current political, social and economic discourse and ‘argument’ is to be found there and while we recognise that there is often no point trying to counter a logical fallacy with logic, we also recognise that we need to be aware of the narrative being set up. And to decide if we see it as an opportunity to exploit, or just noise to ignore. After all, as William James, the father of psychology in the US, once said, “The art of being wise is knowing what to overlook.”

There are a huge number of logical fallacies, but our card highlights the 25 most common ones, which is more than enough for almost all discourse and what passes for argument. Indeed part of the purpose of the MarketThinker substack was to highlight articles and arguments that were broadly accepted and popular, but which rest almost entirely on logical fallacy.

This might make for interesting (or sometimes socially excluding) conversations, rather like the Inconvenientfacts.xyz website which links to both a best selling book and an app with which to counter most of the ‘facts’ presented by Al Gore and others. With no little irony, it is quite inconvenient to access their site via google search and it is blocked by a lot of internet security as ‘unsafe’. But when a prop to the argument is argument from assertion and someone uses government data to challenge the assertions, then a lot starts to fail.

As such, we believe that the bingo card can also serve a number of purposes for investors. In particular, it can help counter a powerful consensus, or bandwagon argument, which relies on the fact that ‘everyone agrees’ - a fallacy in itself, but which has been constructed from a series of narratives which are also logical fallacies. As and when the logic overwhelms the narrative, we see a collapse in the bandwagon and in many cases the bubble that grew up with it.

One example might be Clean Energy; the price of I-Shares Clean Energy ETF that we monitor as part of our Thematic approach went up by 2.4x during 2020 while the number of shares in issue went from 55m to over 300m, peaking last year at 550m. A classic example of a bandwagon effect. However, as the narrative bandwagon builds, so too do flows going into ETF baskets which makes for an asymmetric risk return profile for the stocks in the basket, leading to the emergence of stock specific risk - invalidating much of the reason for investing in diversified baskets in the first place.

The price is now back to mid 2020 levels at around $600, from a peak of $1425 in January 2021, not only as the bandwagon effect of the theme started to unravel, but also because of some stock specific issues. We wrote at the time that we were concerned about the construction of these narrow sorts of ‘Themes’ in particular because we saw them with too much stock specific risk.

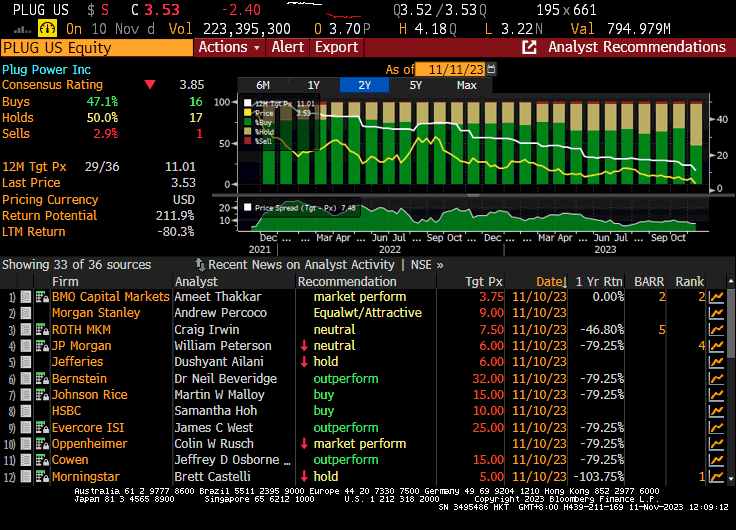

The implosion of Plug Power’s share price is a classic case of bandwagon fallacy delivering stock specific risk

In particular, we highlighted back in 2021 that Plug Power, a green hydrogen company with then a $20bn market cap, was almost 10% of the Clean Energy ETF, as its price had rocketed from $4 to $70 in a little over 6 months. The fact that it raised $3.5bn of Equity and was losing money made us wary of the whole area in fact and we weren’t too keen on $180m of stock based compensation in 2022 either for a company with negative cash flow. Indeed, the fact that the results for the thirteenth straight quarter of losses for Plug Power were even worse than Wall Street analysts had expected is probably the straw that finally broke the proverbial camel’s back. SK of South Korea, the largest shareholder, who bought a strategic stake of 55m shares at an average of $53 is not going to be very happy this weekend.

Amazingly if we look at the Bloomberg Analyst Ratings, (Appeal to Authority on the Bingo Card) we see that despite its share price having fallen over 50% in each of the last two years, there were no analysts on Wall Street with a negative view on Plug Power. Such is the power of the Bandwagon Fallacy. Until it isn’t there any more.

Unplugged - the bandwagon fallacy unravels in Plug Power

This is not limited to Green Energy of course - although this is a key example. More important for investors is to recognise that your returns are based on what you own, not on what other people do. Avoiding FOMO is a key part of investment discipline and the more the Bandwagon builds, the more it becomes self referencing - not least with the share price being held up as ‘proof’ - rather like the appeal to authority of the analysts recommendations.

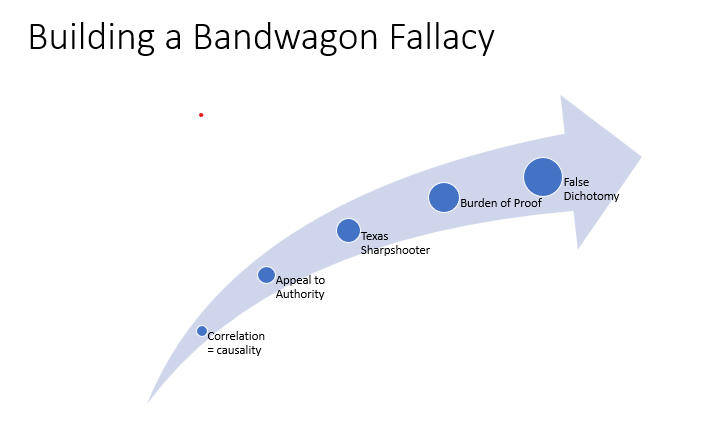

The graphic shows a more generic version of how bandwagon Fallacies build.

Here, by way of illustration, we can see how an ‘argument’ begins with a Correlation = Causality statement (ironically we often find in due course that the correlation is in fact the inverse). That is then bolstered by an appeal to authority and a Texas Sharpshooter cherry-picking of statistics to support the argument. As we approach the ‘everybody agrees’ bandwagon fallacy, we usually see the ‘defense’ of the narrative appear in the form of a ‘thinking past the sale’ tactic of shifting the burden of proof to those disagreeing with the new narrative, effectively requiring people to prove the argument to be wrong, rather than the narrative managers having to ever have proved it to be right. This whole procedure is effectively an ‘argument from assertion’. The next stage may be an ad hom attack, but often takes the form of a false dichotomy as the recommended ‘solution to the problem’, rightly comes under challenge.

It may also lead to other red-herring fallacies like straw men, non sequiturs and deliberate ambiguity, as well as appeals to emotion, arguments from anecdote and feedback fallacies. However, by now the momentum is often lost and the narrative starts to fade. The inherent ‘fallacy of the single cause’ is challenged and with it the momentum of the argument. The narrative begins to collapse and with it the ‘investment solutions’ proposed.

As investors we can choose to ignore the bandwagon, or else to embrace it as an opportunity to be exploited - something that we are used to from watching bubbles form and burst, recognising that Mr Market is being emotional but will likely continue to be so for some time. A form of momentum investing to be sure, but crucially by watching which fallacies start to collapse first, we can see how the logic starts to come through and thus how Mr Market ultimately ‘gets it right’.