Globalists have sold a false premise that the system choice is between Socialism and Capitalism and instead imposed Crony Capitalism. Populism is about to change that.

The West needs more Capitalism AND more Socialism. Although we may not recognise that in fact we just need less Crony Capitalism, Producer Capture and Monopoly Capitalism, the wisdom of crowds can deliver it. 2024 is set to be a year when half the world votes and the rise of Populism means that Globalists will be the targets. Adopting our simple three sector model of the economy to one of the political economy helps us analyse how we got here. And how we might democratically get ourselves back into balance.

Warning; Simplification Alert!

Models are supposed to provide a simplified framework in order to help us understand problems. They are there to provide context and to help us understand some of the key interactions within complex systems. They can help us consider what may happen next, but what they are NOT supposed to be is over-complicated attempts to ‘explain where we are’ in order to predict where we will go next based on the, then, simplified assumptions that every relationship just identified will remain the same. As such, we acknowledge that the framework we offer up below is, by definition, simplified, but that we prefer to simplify at the start and then, in the words of the great economist John Hicks ‘complicate it up a little’, rather than pretend to over-complex models in the first instance and then make simplifying assumptions at the end. As such we do not claim to predict, rather to hopefully offer some value and insight.

The Three Sector Economy

When trying to make sense of the Economy, we have frequently used the notion of the Three Sector Economy, Households, Corporates and Government, with GDP essentially being the flows of capital between them. Economists traditionally look at GDP in terms of Consumption, ie Consumption + Investment + Government + Net Exports (and inventories), or in the jargon, Y=C+I+G+(X-M) +(i). Investors, however, may be more interested in things from the income perspective, ie wages, profits, rents etc, which is to look at the equal and opposite flows from the other direction. Equally, we could try and measure it in terms of output by sector. All three measures are supposed to be equal (but rarely are) but largely we look at it from Consumption, probably because that is easiest to measure (even if it also has huge embedded measurement problems).

Systems not goals

But our aim here is not to measure a goal (GDP) but to look at the system. Thus Corporates interact with Households via Wages in one direction and Consumption in the other, while Households interact with Government via taxes in one direction and benefits in the other. Finally, Corporates interact with Government via Tax and regulation in one direction and Government consumption plus advantageous regulated pricing power in the other.

The role of the Financial sector is then to intermediate the cash flows between these balance sheets of these three sectors. In effect, it adds a third (or even fourth) dimension, time. By allowing debt to accumulate on balance sheets, it enables activity (and thus apparent growth) between the three sectors to exceed that amount of economic activity at any given moment, creating all sorts of distortions and illusions.

For this note however, we have looked at the interaction between the three sectors in terms of the Political process as shown in the adjusted diagram below.

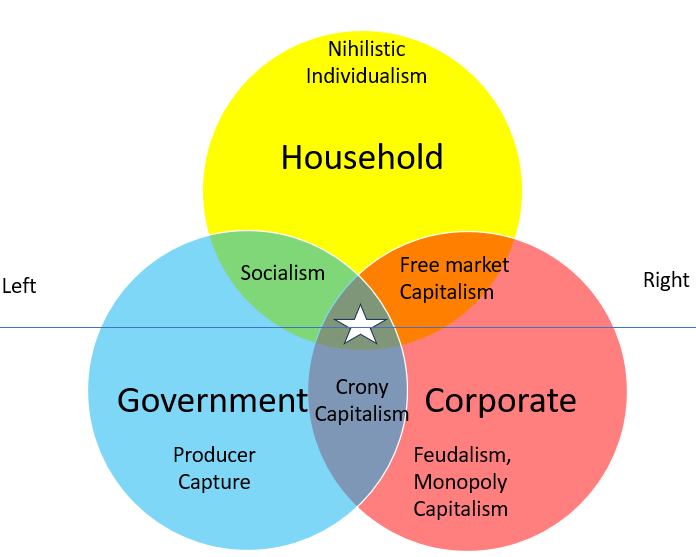

The Three Sector Political Economy

Here we can see that that the interaction between households and Governments is essentially tax in return for public services, specifically the provision of public goods. Different political philosophies will argue as to the exact level/limit of public goods, but broadly we would call this relationship Socialism.

On the other side we have the relationship between the Household and the Corporate Sector, where free markets determine the price of labour and the price of the goods and services provided in exchange. This is what we would refer to as Free Market Capitalism.

The key point here is that the household is Sovereign, the other sectors are there to provide them with their needs and they ‘own’ all the goods and services. The Government has no money of its own, and nor do corporates. As such the relationship between the Corporates and the Government should be to ensure that those goods and services are provided efficiently and effectively. Indeed, we would go as far as to say that this is the true role of ESG, government should be there to ensure the proper pricing of what economists refer to as externalities - the costs absorbed by the general public - and where necessary the regulation to prevent them, e.g. pollution. That is the Environment part. Social is to prevent what, in the words of Adam Smith is the tendency for “People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices.” Preventing private monopolies from forming, and certainly not privatising public monopolies should be the role of a government looking out for the households. This applies as much to the provision of wages as the provision of goods and services. And finally, governance is self explanatory, fairness, a rules based order and freedom from corruption are all key roles for government.

Looking for an Optimal balance

Thus we can re-configure our three sector economy to a three sector Political economy - where we add a “left/Right horizontal axis; the further left we go, the further ‘left wing’ the politics and vice versa. Equally the further out from the Optimal position of the White Star we go, the less optimal things become for the household sector. Left unchecked, the Household Sector might revert to a Randyan even Nihilistic Individualism, while an unchecked Government Sector is subject to what economists call Producer Capture and is run for the benefit of Government itself; the system becomes the Goal. Equally, if left unchecked, the Corporate Sector would impose Neo-Feudalism and Monopoly Capitalism. If all three sectors act as a counterbalance to one another, then (we would argue) we get a balanced society, with both Free Market Capitalism and ESG guided Socialism playing their part.

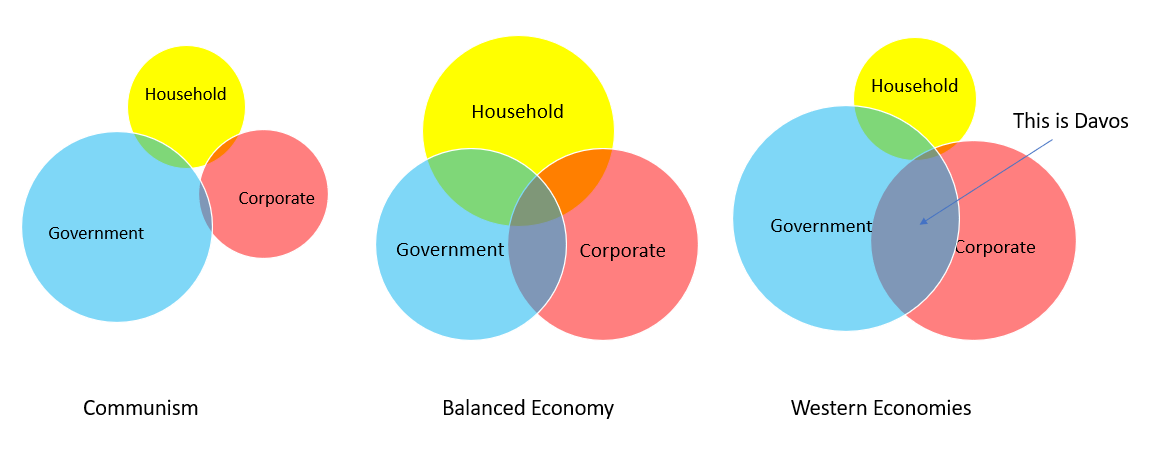

However, that is not what we have across most of the West. Rather, we have the situation as represented in the third panel below, where the overlap between Government and Corporates has become dominant and where the area we have labelled Crony Capitalism becomes dominant.

We would trace this back to the mid to late 1990s and the idea from Bill Clinton’s Democrats and Tony Blair’s New Labour of ‘The Third Way’. Households have lost sight of their Sovereignty as they have been increasingly excluded as the Corporate/Government nexus has grown and as national Governments have in turn been further usurped by Global Government.

The left right axis has been presented as a false dichotomy, it is not a choice between Capitalism and Socialism, there is a pressing case for more of both, but the solution offered by Corporates and Governments to ‘either side’ of the Political divide has consistently been for more Crony Capitalism and more political interference in the economy. Thus ESG has been pushed into boardrooms, incentivising executives to behave like (hugely overpaid) Civil Servants and meet targets and quotas that are political rather than economic and thusrarely in the best interests of shareholders (unless of course they are the board who receive free options to meet these targets). Meanwhile, predatory Global Capitalists have lobbied and obtained a wide variety of monopoly positions and state subsidies to preserve their own ‘excess rents’. We refer to this space in the diagram as Crony Capitalism, but it is effectively Davos and the world of NGOs and Global Government via the UN, the WHO, the EU, NATO and a vast swathe of institutions. It is a world where the domestic household has no power, influence or Sovereignty.

This then is the background for an unprecedented level of upcoming Elections around the world this year and the reason why we chose to start the year by offering this model framework. In our view, the rejection of the status quo that will be termed ‘Populist’ will express itself in demanding more Socialism or more free markets, likely trapped in the false dichotomy that the two are contradictory rather than complimentary. But the result will be the same, a challenge to the ideology of Globalism - Global trade? Yes, Global Government? No.