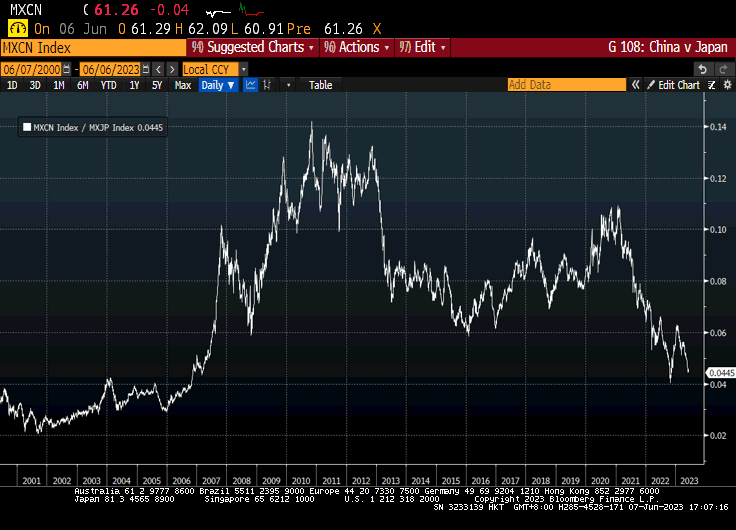

If we include this year to date, we see that China is down for the third year in a row, while Japan is up four years out of five. Partly this may be diversification from the US - it is still the second largest equity market after the US, although back in the heyday it was almost 7 times the size relative to the Global Benchmark, but we suspect that broader Geo-politics and fear that China will become un-investable for a part of the International Investment community that worries about having 'rules' changed on them - be they from ESG or simply new indices to track. Equally, the scars from the 2021 policy decisions on Education Stocks in China - that effectively broke the ADR market have left China risk premia higher (and markets lower). The effect of longer Covid restrictions in China should be out of the system now, so we suspect that this latest bout of relative weakness in China v Japan is more to do with Pro- Japan rather than anti China. Among the reasons we identify is that the 30 years of low interest rates were the drug that was slowly killing the Japanese economy as in over-funded balance sheet Japan they are seen as the return on savings much more than the cost of capital. Thus higher interest rates are counter-intuitively stimulating growth and investors - including Warren Buffet, whose bet on the wholesale and trading companies two years ago only adds to his reputation - are taking notice.

The visualisation of returns from Visual Capitalist shown below highlights all manner of stories, but we would focus on just two - China and Japan.

Clearly, the world has fallen out of love with Chinese equities. They are down three years in a row now if we include year to date. It’s easy to blame Covid and the more draconian approach to restrictions in China, but we think there is more to it than just this. Since Xi called time on the ‘Shrodinger’s cat’ concept of ADR’s back in mid 2021 (they were deemed to be simultaneously 100% Chinese and 100% foreign owned, a form of magical thinking that was fine, until it wasn’t) China has become ‘un investable’ for many western investors. This has created ‘bear market conditions’ for many of the ADR stocks since then. By this we mean all rallies are sold as stock shifts from weak hands to strong hands. This is something we discussed in our recent June Market Thinking.

Thanks for reading Mark’s Substack! Subscribe for free to receive new posts and support my work.

By contrast, Japanese Equities are up in 4 out of the last 5 years (again if we include year to date) putting them now in fourth place on a 10 year annualised basis. Indeed, since the start of Covid, Japan has outperformed China by almost 50% in $ terms. So what do we think might be happening?

Japan outperforming China since Covid

- Covid is an obvious factor - the lockdown period was far longer in China than the rest of the world and the huge uncertainty premium left China economically un-investable for many - or at least “too difficult”. This of course should no longer really be a factor - certainly not to explain the 20% relative performance since January (almost 30% since February).

- Geo-Politics is definitely a newer factor, both in selling China and in buying Japan. The former is now deemed politically rather than economically un-investable by an increasingly large proportion of western investors, especially those who are what we would term ‘Fiduciary’, large institutions such as pension funds and insurance companies, where trustees are concerned about being forced to sell if ‘the rules’ change. In this there are strong similarities to the effect of ESG on energy and mining stocks. Indeed, on the Market Thinking blog back in 2021, we described ESG as a Trojan Horse (see Trojan Horses and Slippery Slopes ) for ongoing political interference in capital allocation.

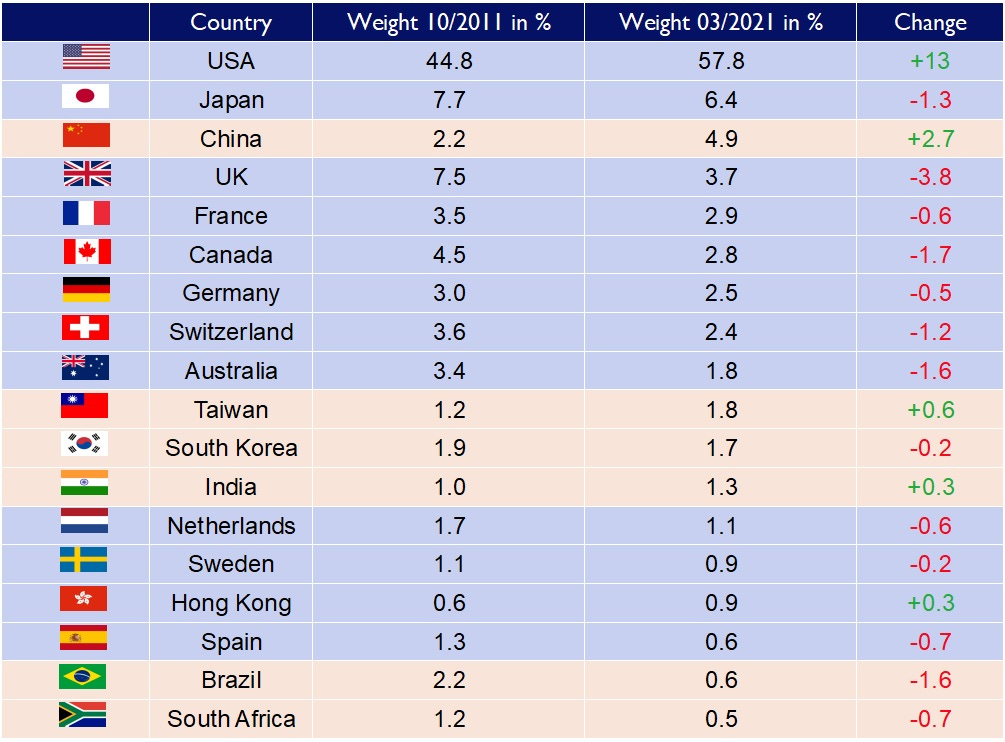

- Index weighting. Japan is seen as the largest alternative market for Asian investment flows - sorry, but for all the (perpetual) hype around India, most long term investors remain extremely nervous for a variety of reasons, not least size and liquidity. The table shows the shift in weighting in the MSCI All Country World Index over the last decade - India, along with China is one of the few to have increased, but is still only a 1.3% weighting.

- Amazing that even though Japan is still number 2, it used to have 6 times the weight it does now

- The standout from the table of course is the massive increase in the US weighting. Back in 2011, at 44.8%, the US was already as large an index constituent as Japan had been at its peak in the late 1980s. Now, at almost 58% it is crowding out a lot of international investment opportunities.

Geo-politics meets Index Weightings

Source MSCI.com

- Inflation and interest rates. This might not be the most obvious, but in our view is the most interesting. It is consistent with what we are seeing in the other direction in Europe and the US. For 30 years, low interest rates did not boost spending and inflation but the opposite, they reduced spending and increased saving in Japan for the simple reason that the Japanese see interest rates as the return on savings, not the cost of borrowing.

Models based on a Consumer Borrowing culture like the US, work equal and opposite in a Consumer Saving culture like Japan

Of course, all computer models seem to be based on the premise that what happens in the US happens everywhere else - hence the false belief that lower rates lead to higher borrowing and spending always and everywhere.

Higher rates in Japan actually achieving what 30 years of lower rates did not

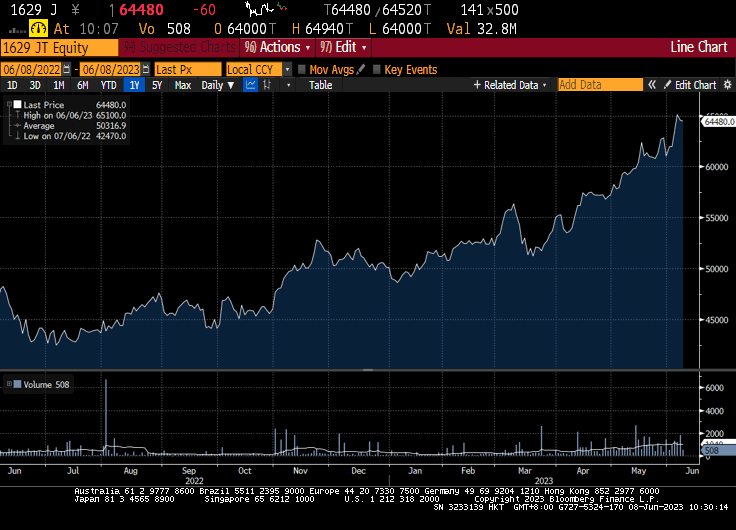

Another factor is that investors are recognizing that Japan, having been a good way to play not only themes like Robotics and Automation (one of the themes in our long term portfolios where Japan is 17% of the fund, more than double the MSCI ACWI weighting mentioned above) but also a play on economic growth in Asia. As we have discussed in the past, the ‘Buffet Trade’, buying the Japanese trading companies remains a winner. He borrowed extremely cheaply in Yen and bought a collection of companies like Itochu, Mitsui, Sumitomo and Mitsubishi Corp, all with yields over 3%. We can monitor this with a good proxy in the Commercial and Wholesale trade Index, shown below as the tracking ETF 1629 JP

The Buffet Trade continues to work in Japan

Easy to understand, offering carry and a macro theme, its starting to attract a lot of attention.

This is also available on the substack marketthinker.substack.com. Subscribe, it's free!