After a very strong July, August has been a difficult month for asset markets, with most, if not all, of the previous month’s gains reversed. This has come on the back of a first half that was flat for many factors and themes, and by extension many equity investors, with the benchmark indices heavily distorted by the rebound in “the Magnificent Seven’ mega cap tech names. July had seen the markets ‘broaden out’ and, as such, for most investors those July gains had made up the bulk of their returns year to date, meaning most are now once again ‘flat’. A frustrating case of two steps forward, one (or even two) step(s) back. At the same time, the megacap tech stocks saw modest profit taking that nevertheless meant double digit percentage drops, with many eyeing the safety of a 5% yielding money market fund to lock in some positive returns for the calendar year.

We remain of the view that while we have avoided the widely predicted second leg of a bear market, that is not the same thing as saying a new bull market has begun. Retail sentiment had become overly bullish in the US during July, which is often a short-term contra-indicator - and that has now reversed - but the foundations of a proper bull market will depend on institutional investors moving out of their heavily overweight cash positions into equities in search of real returns. For now, the high returns on cash are making that a decision that is easy to delay such that a clear indication of a peak in cash rates is likely to be the necessary catalyst.

Deliberately or otherwise, the high returns available on cash are sustaining a liquidity drought across other markets.

Short Term Uncertainties

We would date the turn in equity sentiment to the late July Bond market sell-off in the wake of the announcements by the Bank of Japan on the ‘beginning of the end’ of Yield Curve Control. Interesting to note that this appears to be hitting Equities via economic confidence rather than working through valuations and as such it is the shorter duration themes in our model portfolios like mining that have suffered more from the bond selloff than the longer duration technology related, ones like cyber security. From a technical viewpoint, it looks like early August saw a lot of traders’ stop losses triggered and with many traders ‘heading to the beach’ and institutional investors still on the sidelines, prices have had to adjust to levels where longer term value investors begin to appear.

The likely trigger for the equity reversal was the Japanese/US bond sell-off in late July, while the mechanism was the tripping of technical stop losses for traders who were already heading to the beach

Traditionally, August seasonality is not good and September is even worse, with the mid month options expiry often a key point for asset allocators looking to position for the fourth quarter, so sitting on the sidelines is likely to remain the near-term default position for risk managers while the traders are likely to try their luck pushing on the down side. In the meantime, the macro narratives tend to dominate, with not only a focus on when cash rates will peak, but also a lot of geo-political manoeuvrings taking place, especially with regards to Asia and the BRICS. While there is currently a lot of ‘noise’ around China, in many ways one of the biggest near-term uncertainties is Japan. With the 10 year bond yield at 10 year highs and both inflation and economic activity rising, Japan’s long-held role of capital provider to the west may become increasingly challenged. This, in our view, is an issue for longer dated US Treasuries, especially as other traditional buyers, notably Sovereign wealth funds, are diversifying away from Treasuries and the role of risk free asset is being taken by US$ cash. This appears to be helping the $, but not the bond market.

Medium Term Risks

In the August monthly, we noted that China represented a long term trend that should not be ignored, not least because the shifting composition of its own economy represented both an opportunity (consumers) and a threat (higher value added exports such as EVs) to existing portfolios. During the month we added a further post highlighting the (to us) very obvious shift in the narrative to present China in as bad a light as possible, highlighting a number of already well known long-term issues while seemingly ignoring similar (or worse) problems elsewhere, shifting the issue of China from a long term trend to a Medium Term Risk.

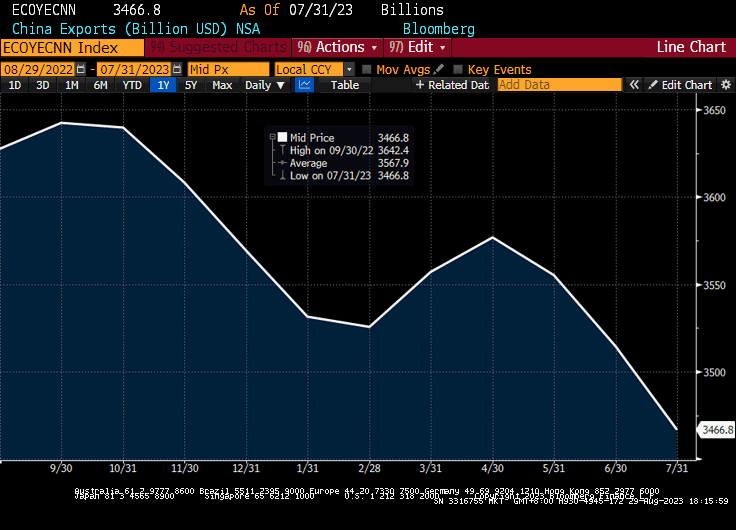

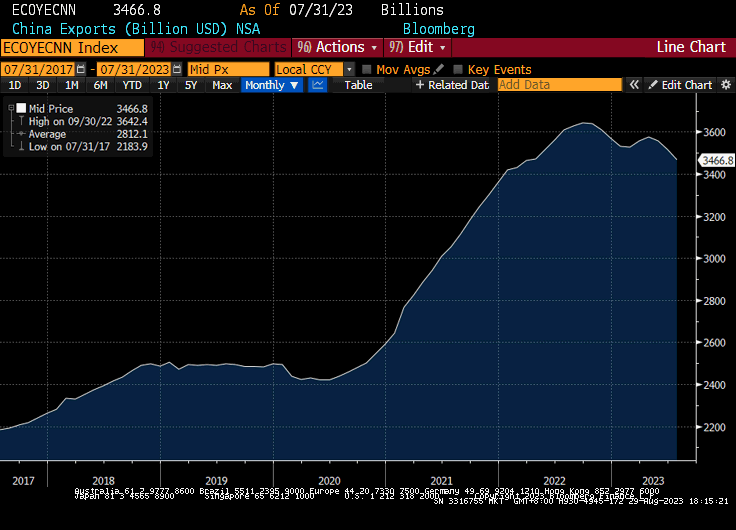

We note in particular, that, exactly two years after the shock to the Chinese education stocks and the undermining of the ADR markets, a lot of long-only international money is now being pulled from China, seemingly worried about sanctions and possible ESG style limitations on ownership. A negative economic narrative has appeared in support of this, one that is also supported by western politicians keen to diminish the appeal to would-be BRICS members of a Chinese approach to economies and markets. However, from an investment point of view, we would note that the data supporting this narrative is neither new, nor very convincing. China’s property sector is de-leveraging for sure, but it has been doing so for the last two years and while painful, certainly for those speculating in its offshore bonds, is not a systematic threat. Equally the story about youth unemployment is not new and is undoubtedly a factor in the previously announced supply side reforms. However, it is the narrative on exports that is the weakest. While they are down on the last three months, they are actually up 40% from pre-covid levels and with a much higher value added component.

A question of Context

China’s exports this year

China’s exports over the last five years

These negatives feed into an ongoing western narrative that the Chinese economy is dependent on either exports or building/infrastructure, ignoring the fact that it is shifting to an increasingly domestic-focussed consumer led economy - albeit not one driven by credit expansion. Investors should focus on these areas that are growing and driving China’s 6.5% GDP growth, three times the current run rate for the US and ten times that for the EU, (this is in real, not nominal terms of course) and also recognise the competitive threat that China represents to many western companies that may be in existing portfolios.

Meanwhile, the focus will shift over the next quarter to once again ask the question “where am I going to get a real return and compound growth?” The answer of course is in growth equities, which is why we need to concentrate on where the growth is coming from at the sector and theme level, rather than focusing on high frequency macro data. Importantly, it won’t be coming from cash for much longer and the minute the markets sense that ‘the Fed is done’ asset allocation will switch.

Long Term Trends -

Beyond the short term narratives and the medium term crowding-out effect of the inverted yield curve, the new ‘New Normal’ of economies and markets in a ‘post Zero’ world continues to emerge. While ‘normal’ levels of interest rates are undoubtedly a factor in the Chinese real estate problems currently being highlighted (the forward selling to fund future projects is a bigger issue), they are even more important in Europe and the US and while the liquidity logjam will ultimately become freed, the business models around much of these illiquid investments are increasingly challenged - and not just by the reduced willingness to give up liquidity.

Higher interest rates are redistributing economic activity more rapidly than many realise

While much of the focus of the impact of higher interest rates has been, understandably, on those with high borrowings, we have an interesting phenomenon emerging where households, corporates and, indeed, states, with strong balance sheets are now getting a return on their cash for the first time in decades, and this is starting to affect demand and supply for a variety of goods, services and indeed assets. Cutting returns on savings for Japanese households did not lead them to borrow and spend more, but raising returns is - a point so obvious that only a central banker could miss it. Meanwhile, many large corporates have either got long term bonds at fixed rates and are running a carry trade into 5%+ US cash, or have no debt at all and are similarly seeing their balance sheets generate healthy ‘operating profits’ and in many cases throw off enough cash to pay higher dividends or buy back shares.

Finally, cash rich (mainly resource rich) countries are in a similar position, which is why the invitation for Saudi in particular, but also UAE to join BRICS is so important. Saudi has ambitious plans for its economy - including building a $500bn mega city called Neom in the north of the country - and is already making its presence felt, not just in sports like Golf and Football, but in the professional service areas (PWC for example are all over it).

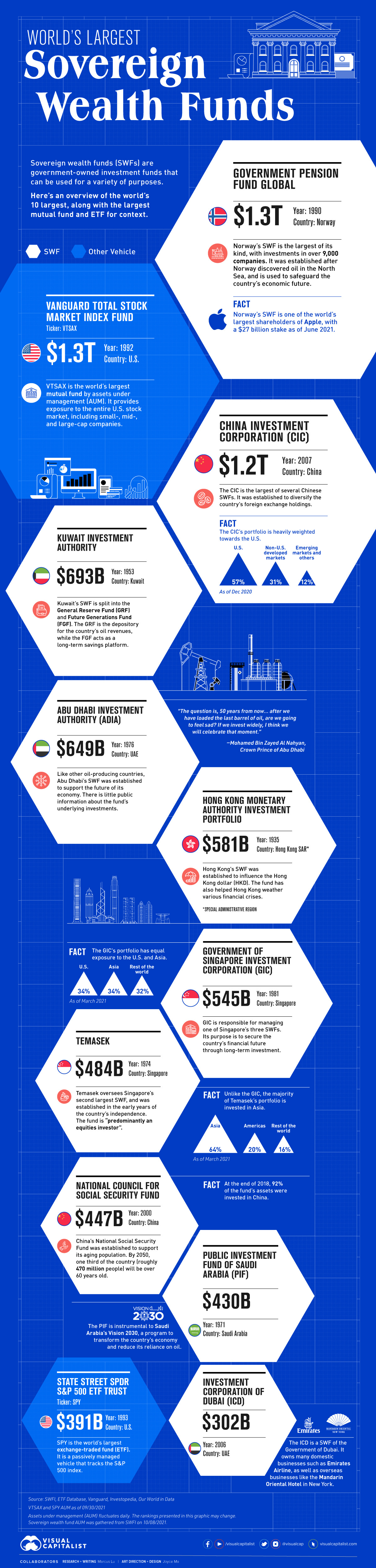

As we repeatedly say, de-dollarisation is about diversification away from the US Financial system, it is not about replacing the US$ as a Reserve Currency. However, if we were to look at the graphic from the ever-excellent Visual Capitalist, we can see that more than 2/3rds of the assets of the largest Sovereign Wealth Funds are now effectively in BRICS and that the old model of recycling domestic excess savings via purchasing US Treasuries and thus allowing the US Financial Markets to allocate investment capital is being over-turned. The new BRICS grouping announced this month includes not only the UAE and Saudi, with their large SWFs, but also Argentina, Iran, Egypt and Ethiopia (the latter two being some of the most populous nations in Africa). This group now represents 37% of world GDP in PPP terms (G7 is now down to under 30%), about the same as the percentage of the world’s landmass, almost half (46%) of the world’s population and, in many ways most significantly, 54% of the world’s oil production. With the likely incorporation of Algeria, Venezuela and Kazakhstan as early as next year, that would extend to a near total monopoly on Oil and gas traded globally.

From a markets point of view it also represents a large source of excess savings that will likely no longer be recycled through the old Petro$/Washington Consensus system.

Building an Alternative Capital Market BRIC by BRIC

The days of SWFs buying Treasuries or investing in REITs or Private Equity groups that locked up liquidity for many years in other countries are, if not completely over, then unwinding rapidly. Unless they traded actively and sold in 2020/21, anyone who bought US long bonds since 2016 hasn’t seen a positive total return and those who locked liquidity up in ‘alternatives’ are unlikely to want to repeat the exercise. For now, they are undoubtedly happy with US cash at 5% - which is helping the $ - but that is not a long term plan. The Belt and Road Initiative is putting the BRI into BRICS and to a financial world brought up on the Petro $, the IMF, World Bank and Washington Consensus, that is going to be a profound shift in economic power.

Please note that none of the above should be considered investment advice. it is for information and hopefully sometimes entertainment purposes only. Please consult a financial advisor before making any investments.