Central Bank Orthodoxy is all about managing demand through interest rates. Not only does this not produce the desired effect, it has actually produced the opposite of what was intended. Mainly this is because it has a greater impact on supply. Low rates increased supply and brought dis-inflation, now higher rates look to leave inflation in a 2-4% rather than a 0-2% band. Same policy error, just opposite direction, Bond vigilantes, meanwhile, always looking to support their markets are demanding ever higher rates to drive inflation to zero by completely collapsing demand. The wider economy, as well as equity markets have to hope they are not listened to.

So, the Bank of England has increased rates yet again, effectively taxing the disposable income of the working age classes in order (apparently) to ‘fight inflation’.

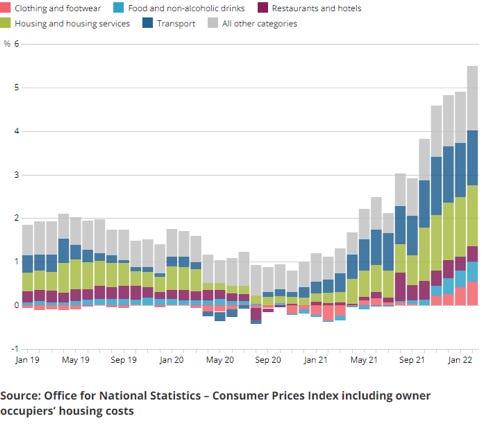

Here is an image from a recent (March) report from the ONS on the main drivers of UK inflation (link here) and we can see that they include Food and non alcoholic drinks, transportation costs and housing and housing services. Together these make up the majority of the CPI, with the latter two making up over 50% between them.

And yet these are all effectively essential goods, they will be prioritised over everything else. As a result of this simple fact, the policy of targeting aggregate demand to reduce these prices is a dangerously blunt instrument. Everything else will go first.

Trying to curb the price of essential goods by increasing the cost of borrowing - as is the orthodoxy- will, almost by definition, affect the price of everything but these variables.

Even more absurd (if we are to think about it) is that by increasing the cost of mortgages so rapidly and dramatically we also increase the imputed rent component of the housing and housing services component. Our ‘cure’ for high prices is to raise prices!

Then when we look into the housing services component we see that this includes utility costs, which have of course gone up dramatically thanks to a combination of government policies on Ukraine and Green Energy - in fact, the consequence of a series of bad policy decisions long in the making that have left the UK with no coherent energy policy and a monopolistic supply side.

Central Bankers focus almost exclusively on trying to manage demand, largely ignoring the importance of supply. Indeed, ignoring the fact that their policies often have a bigger impact on supply. Usually in the opposite direction to their intention.

And this is the fundamental issue; the central bankers are obsessed with controlling prices through interest rates by boosting or restricting demand. This has three fundamental problems; first that it assumes that lower interest rates actually do encourage more borrowing and spending - which might be true in a borrowing culture, but not in a savings culture. Second that any new borrowing will go into consumer spending rather than asset purchases. The third and perhaps key point, in our view is that they seemingly make no assumption about the supply side of the equation. And it is supply that has been most affected by monetary policy.

So, we end up with a situation where, over a decade of QE and ultra low interest rates had produced dis-inflation on the high street but a huge rise in asset prices. Meanwhile, 30 years of low interest rates in Japan had simply increased saving rather than borrowing. And yet, nobody thought to question the orthodoxy.

Nor, seemingly, is anybody acknowledging the fact that, as per Monetary Theory, a huge fiscal stimulus during Covid that was monetised by the central banks stimulated actual demand for goods and services at the same time as zero Covid policies collapsed supply, leading to the (accurate but much mocked) transitory inflation of 2022. Unfortunately, the rapid response by the Central Banks to ramp up interest rates to reduce demand has instead put further downward pressure on supply as smaller companies went bust, extended supply chains were permanently shortened, zombie companies were allowed to fail and the high rates on cash sucked all available liquidity out of capital markets.

Meanwhile, the Bank of England seem to have now decided that they are worried about ‘wage-price spirals’, another look-back to Keynesian demand management from the 1970s (that didn’t work then either). Higher wages lead to higher prices in areas where there is no competition - i.e. limited supply - the very conditions the BoE’s policies are creating!

Structure of Balance Sheets

Over 20 years ago, I held a seminar when I was an Equity Strategist at UBS Warburg called something along the lines of “The importance of Balance Sheets and why everything you know about interest rates is probably wrong”. A punchy title to be sure and one that certainly upset the Bond economists, but the point being made then, as now, is that, just as with company analysis, the impact of a change in interest rates can not be analysed with reference to what has happened, on average, in the past over a range of samples with wildly different balance sheets. Nobody would claim to estimate the impact of higher interest rates on, say, the cash flows of a German industrial company with reference to the average impact on industrial companies in the UK and the US over the last 50 years, and yet that is exactly what the economic models try and do. Countries with high levels of consumer debt that is floating or only short term fixed, like the UK and Australia, will have markedly different reactions to higher rates than countries with low levels of mortgages like Germany or fixed rates like France, let alone Fixed and re-financeable like the US. But policy makers don’t seem to ‘see’ this and persist in effectively raising the ‘tax’ on disposable income in their quixotic attempts to control demand.

The truth is that in countries like UK and Australia, Monetary Policy effectively acts like Fiscal policy

Put this way, it would (rightly) seem ridiculous to suggest that the best way to deal with the cost of living crisis would be to increase taxes on consumers, and yet that is effectively exactly what is being done. The fact that most of this cost of living crisis has been caused by actual taxes being put up - be they income taxes, Green levies or geo-political inspired tariffs only adds to the irony (or sense of frustration).

Bottom Line

Zero interest rates did not spur inflation by boosting demand, in fact they spurred dis-inflation on the high street by boosting supply. They did however, spur inflation in asset prices. Inflation ultimately occurred because of Zero Covid, which simultaneously restricted supply and boosted consumer demand through a massive fiscal boost that was monetised by central banks. Unfortunately the orthodoxy remains unchallenged and is now making the same error in reverse.

Higher rates are now hitting asset prices and ending dis-inflation, as supply chains collapse, smaller companies and zombie companies go out of business and larger companies seek to maximise profits. So just as low rates caused lower prices, high rates are causing higher prices. The UK is getting harder hit than most due to a combination of, previously very competitive, markets for goods and services such as super-markets and airlines becoming more monopolistic and the much higher level of sensitivity to short term interest rates due to the mortgage position of UK households (highly leveraged compared to most with only short term fixes). Supply down, taxes up and demand down risks stagflation. Throw in an incoherent energy policy and a mechanistic monetary policy that actually both contribute to the very price rises they are trying to ‘cure’ and the situation is far from encouraging.

Talk on the asset price inflation, now deflation, is currently mainly focussing on Housing, but should also include bond yields, since the equal and opposite effect of this round of monetary policy is that with dis-inflation gone, we should expect inflation more in the 2-4% band rather than 0-2%. Also, in the UK the fact that the Government expanded to over 50% of GDP during lockdown and has not shown any signs of shrinking, further compounds the supply side of bonds as well as the demand side. Much of the push for higher rates is, of course coming from the Bond Economists, citing the need for ‘credibility’ when what they really mean is they want a recession to support bond prices. Previously austerity was good for Bond markets and QE was even better. Following a terrible year in 2022, there is a rush to lock in higher yields to meet asset liability targets, but that then requires a collapse in economic activity and prices.

The Bond markets want a recession to support their market. Equities have to hope they don’t get their way

As we have said before, many emerging markets, especially in Asia, have not had this series of self imposed problems of the wrong level of interest rates, ever rising taxes and an incoherent energy policy. With no sign of western central bankers and policy makers acknowledging, let alone accepting their previous errors, at a minimum, investors should consider some diversification.