Every year, for as long as we can remember, we have written a weekly or a monthly note with some variation of the ‘Sell in May’ trope, so we see no reason to break the habit this year. The chart (courtesy of Nick Glydon and team at Redburn Atlantic) shows the steady uptrend in searches for the expression every April over the last 14 years and while obviously there is a ‘usage factor’, it is certainly on a lot of traders’ minds at the moment. The historic rationale for the expression comes from the leveraged trading end of the spectrum and tended to reflect the fall in speculative activity in the commodities markets over the summer months and while the speculators have moved heavily into other markets since those days, the seasonal drop off in activity as the head traders head to the beach remains a factor - the juniors tend to flatten the books and keep things ticking over. It tends to mean bear markets worsen while bull markets tread water. Given we see bonds in the former and equities in the latter, we would expect this to be the case over the next few months.

April is therefore often a month for trying to establish where the summer trading ranges might be. Thus we have seen most of the Magnificent 7 sell off and ‘bounce’ off something close to their 50 day moving averages, with the M7 index now in the middle of a + or - 10% range. Individual stocks too have moved in large ranges, notably Nvidia, which at one point was down 16% on the month, before closing 3% down. Tesla was at one point down almost 20%, before being up over 20%, ending at around +16% , while short covering also led to Google spiking almost 10% at month end.

The short term inflation/rates panic mid month has subsided and the slight hysteria over interest rates rising rather than falling has also eased back. Commodities, notably Oil, which picked up some speculative activity on an inflationary trade are also taking some profit and may well be the area where the Sell in May trade does appear. The industrial metals, notably Copper, however, remain in a bull trend.

The main exceptions were Hong Kong and China, which had not only missed out on the general q4 rally but had also seen geo-political risk management related sell offs. These saw the steady recovery since their January lows continue into April, with suggestions of an end to the distressed selling and a shift from ‘weak hands to strong hands’.

In our model portfolios we see most of our themes as now equal weight, except for Gold and Mining and Energy infrastructure, which have established some new bull trends. Within factors, we see Quality as currently the most favoured, with momentum in particular running out of, well, momentum and having had a pull back in April. In fact, the Global Momentum Index has just corrected a Fibonacci 23.6% of its rally since last September.

Short Term Uncertainty - trading ranges

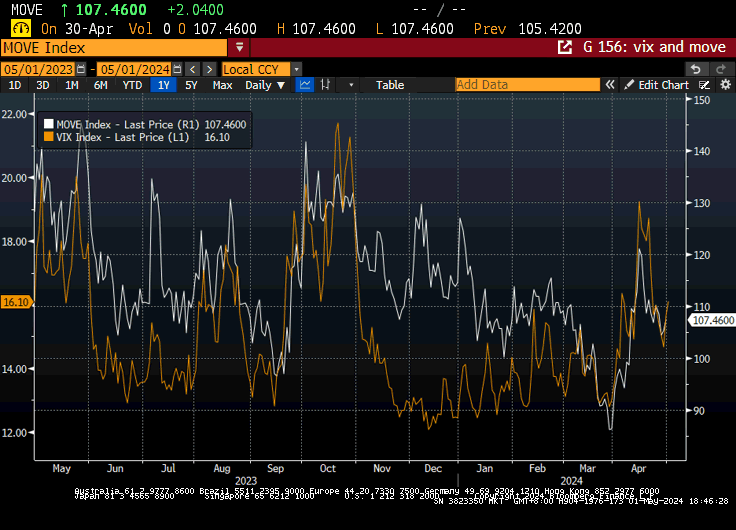

Strong momentum tends to keep volatility lower than it otherwise would be, so with the momentum factor fading we would expect volatility to rise somewhat in the near term, something that the Fed will be watching closely. In particular, we believe that the Fed will continue to quietly monitor the health of the bond markets as a key variable in setting rates - over-riding the pundits’ obsessions with wages and employment costs. As such, the Bond Volatility Index (MOVE) is now being closely watched - shown here with the VIX, the equity volatility index that was a previous focus of policy makers.

Bonds, increasingly just another volatile risk asset?

We can see that both indices spiked higher in mid April around the time of the inflation report, before settling back down again. The graph also illustrates the problems facing the traditional 60:40 model - bonds are no longer acting to provide diversification in either returns or volatility. They appear to have become simply another risk asset. As previously discussed, we think Gold is increasingly taking on the role of the ‘risk off’ asset.

While the more options heavy stocks like Tesla and Nvidia had a volatile April, it was interesting to see that the biggest of the Magnificent 7, Microsoft, was more conventionally weak over the month, while Meta, having been steadily weaker dropped almost 14% in a single day on disappointing guidance (maybe we should have paid more attention to Zuckerburg selling half a billion dollars of stock at the end of last year? ) generally supporting our suspicions that the AI trade is fading and the may be the other place apart from Commodities that the Sell in May trade may have some legs.

June sees the European Elections, with much ‘concern’ in the media over so called ‘far right populists’ - a phrase used to described anyone disagreeing with the Globalist paradigm of open borders and Net Zero. From a markets point of view, resistance to the latter is probably more relevant and while this is part of the growing benign neglect of ESG (everyone is now trying to pretend they weren’t quite as enthusiastic as they once were) we would note that, sadly, this is unlikely to mean less tax and spend - and by extension a better off consumer. Instead governments are simply switching their closet industrial policies elsewhere - notably defence.

Geo-politics is never far away, and with May day and other celebrations in Russia , many are understandably nervous about escalation for propaganda purposes, which in a market currently moving huge cap stocks + or - 10% a day, will likely add to the desire of many traders to take some money off the table for the summer.

Medium Term Risks -From Green to Camouflage

In the UK, we saw previous governments try and co-opt Climate Change as industrial policy with the elusive ‘high paying Green jobs’ and now we detect a clear shift to Defence spending, hoping to achieve the same thing. The US is, of course, encouraging European countries to boost their contribution to the vast Pentagon Budget under the guise of NATO, which means that rather in the way that European spending on Climate Change ended up boosting China, so European spending on Defence will end up boosting the US, as, with energy self sufficiency, US Foreign policy now appears to be as much about generating exports as it is about securing imports.

Guns, Gas and Grain are all now key US exports.

Meanwhile, in anticipation of a Trump Presidency, the US Military Industrial Complex (MIC) is doing its best to future-proof its access to government funds - which sadly means more bellicosity on multiple fronts, as ‘threats’ are identified in land, sea and air to satisfy all providers of ‘solutions’. The problem more generally for markets is that Military spending, like ‘Clean Energy’ is ‘stagflationary’, primarily because it diverts resources to less productive areas, money literally goes up in smoke and of course a key insight is that jobs are a cost, not necessarily (or even usually) a benefit. We have what the French Economist Bastiat referred to a ‘what is seen’ (jobs in Green energy or the MIC) versus ‘what is unseen’, the high speed rail, or the high speed internet or the nuclear energy (or any manner of things) that didn’t get built. Equally, the jobs that are lost as the increased cost of green energy drives companies out of business. Bastiat’s example was the parable of the broken window , where ‘work’ is created by a window being broken and then being fixed, with the logical conclusion that if this was a ‘good thing’ then the entire economy could exist on breaking and repairing windows. Or, of course, wars.

Similarly, global trade with China was good for both growth and inflation, but politicians shutting that down to ‘create jobs at home’ exchanges one certain benefit lost with a highly uncertain one to be gained.

Meanwhile, what is probably the biggest anomaly at the moment - and by extension one of the biggest headaches for asset allocators - is the Japanese Yen. During April, as everything else sold off and then mean reverted, the Yen did not. It just sold off. As previously discussed, the problem with the Yen is that there is so much ‘stock’ of Japanese cash in international carry trades - usually hedged back to the Yen - that the currency moves are almost always a function of market mechanics rather than economic fundamentals. Currently there are hedges going the other way as a popular strategy is to own the Japanese equity market hedged back into US$, (which may even be driving the Yen). Should the Yen start to strengthen, these hedges may be taken off and exaggerate the moves in the currency, as would the Japanese money currently running carry trades into EM bonds.

Long Term Trends - trade

The latest moves by ‘The West’ to confiscate the frozen Russian assets are another step in the direction of de-dollarisation for ‘The Rest’ and is undoubtedly a feature in the recent strength of Gold - China is buying commodities, especially energy, in Yuan and offering the option to exchange to Gold on the Shanghai Exchange, so obviously the more the trade grows, the more Gold is needed to support this. It also means that Chinese exports are increasingly going to focus on those markets with excess Yuan and also to manage the exchange rate against this basket rather than against the $.

On the one hand, this activity to apparently undermine the $ may look like a mistake by the US, but there is a theory that in fact the US actually wants the rest of the world to stop using $’s to buy oil; if the price of Oil, or indeed the $ spikes, then countries will be forced to sell $ assets, principally Treasuries, in order to buy their energy. As noted last month, foreigners have gone from around half of the buyers of Treasuries to around a third and while the stocks held may not have gone down much in recent years, the percentage of the outstanding has dropped sharply as issuance has ramped up. Five years ago, US debt was around $20trn and foreign central banks owned around a two fifths of it. Now they own around a quarter and so far this year the US has issued an amount equivalent to almost the entire holdings of Foreign central banks. The last thing Janet Yellen wants is for those Central Banks to be selling their holdings into a market already struggling with supply from the US government.

If such logic holds, then a weaker $ would also be in the interest of the US, especially as it is now looking to boost its exports, so we might get some attempts to talk the currency down - especially against the Yuan and the Yen.

This time a year ago, the apparent weakness of Chinese exports was being cited along with the housing market ‘collapse’ , the under-performance of the Chinese stock market, the (somewhat niche) youth unemployment data and the shrinking population as one of the ‘five reasons’ why China was ‘imploding”. As discussed previously, most of these statements bear little scrutiny, especially in a relative sense - for example, the youth unemployment is high, but is for a relatively modest element of the working age population, unlike in, say, India. The housing market we see as being a controlled demolition of the developer bubble (it just happened to hit western investors hardest), the stock market, while not actually being a big deal for Chinese consumers, is recovering and a shrinking population needs to be looked at in terms of GDP per Capita, the target that the Chinese actually use.

In trade, the consensus is now for net exports to be a driver to the 4.8% growth forecast for this year, especially to BRICS countries. And driver is the operative word, China has gone from a country with ‘nine million bicycles in Beijing’ to the biggest manufacturers and exporter of cars in the world in less than 20 years. This will continue to be a source of tension with the US and Europe which have recently started up accusations of dumping, but the reality is that while demand for Eur100,000 Teslas or electric Porsches and Audis may be stalling, demand for Xiaomi’s Eur30,000 Taycan clone/ Tesla equivalent or BYDs Eur13,000 equivalent of the Eur35,000 electric Fiat 500 is enormous.

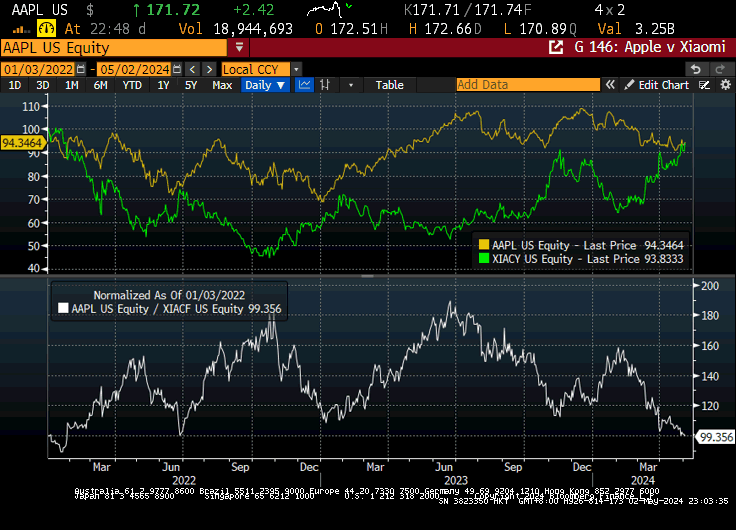

How do you like them apples? Apple versus ‘the Apple of China’

When Xiaomi floated, it was promoted as ‘The Apple of China’. As the chart shows, it didn’t start well for the phone maker, but now, helped by the launch of its SUV 7 Taycan look alike, it’s caught back up again. Anecdotally it also makes a wide range of high quality, elegantly designed and amazing value consumer electricals with Apple style packaging. Even on the UK website things are good value, but in Hong Kong they are almost 40% cheaper still. While on the one hand this means good export potential (assuming it is not blocked by tariffs), the really important point is that the ability of western companies to export into Asia, let alone China, is going to be seriously challenged.