January saw the predicted return of politics to markets, not just with Donald Trump now looking certain to be the Republican Candidate, but with a greater sense of fracturing across the West as populist protests against Globalist policies of Green levies and immigration continued to rise. The Taiwan Election was touted as a ‘win’ for anti China sentiment even though 60% of votes went to parties that were more pro- Beijing, while the EU Elections in June threaten a similar lack of mandate for continuing the Globalist policies. With Elections coming up across much of the world this year, policy U turns remain one of the primary sources of uncertainty this year.

Short Term Uncertainties

Bonds markets, having got somewhat over-extended on ‘pivot’ talk at year end, backed off as we expected during January, with the more excitable fringe reining expectations back in and establishing what looks like a 4-4.5% range for the 10 year yield.

Index effects continue to favour momentum and tech stocks, essentially NASDAQ over SPX, with Tech stocks like Nvidia and Meta continuing to charge - although Tesla has dropped sharply. The equal weighted S&P is essentially flat, as it was largely in 2023 - leaving a lot of people who were actively invested outside of the Magnificent 7 a lot less excited than those who were.

Stock Markets are another example where most people don’t actually think like the US does

The stock market is seen as a measure of economic success in the US, by politicians and pundits alike, reflecting the middle class habit of 401k pensions as well as the widespread use of options in remuneration schemes. A healthy stock market is seen as meaning a healthy economy and this undoubtedly has contributed to the concept of the Fed put. Far less so in Europe and even less in Japan, who cut rates in response to the Fed not to support their own stock markets, something that should be borne in mind when linked to expectations of the need for the authorities to ‘do something’.

Most obviously this applies to China, where the glass remains decidedly half empty so far this year, with the Shanghai Composite continuing to make lower lows, challenging the 2020 lows, as every rally is sold. The bounce ahead of Chinese New Year is to be welcomed, but not yet trusted.

Hong Kong meanwhile, broke the 2020 lows a long while back and while the (final) suspension of Evergrande this month at 16c had minimal impact at the index level, the fact that so many westerners were holders of its (almost equally collapsed) competitor Country Garden continues to give a far greater importance to both the Chinese Property sector and indeed the stock market in general in the minds of overseas investors. It’s not that the Chinese authorities don’t care about the stock markets, indeed, they widely telegraphed what they were going to do in the property sector two years ago, as we discussed in November Market Thinking. Its just that western ‘investors’ seemingly chose not to listen.

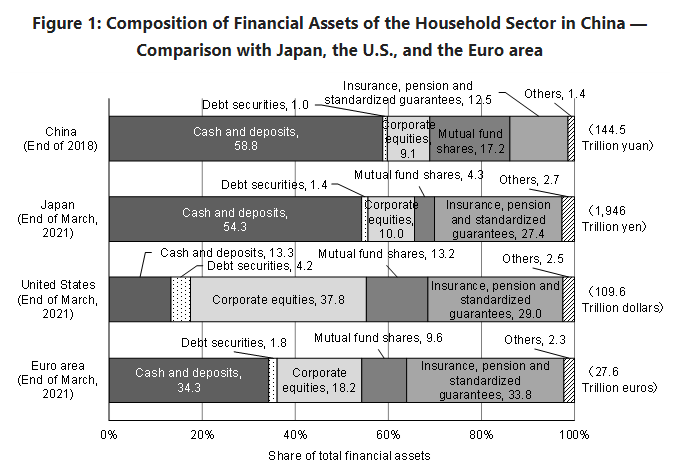

If we look at the graphic (from a Japanese economic think tank), we can see the difference in household sector assets for China, Europe and Japan versus the US.

Source: Research Institute of Economy Trade and Industry, Japan.

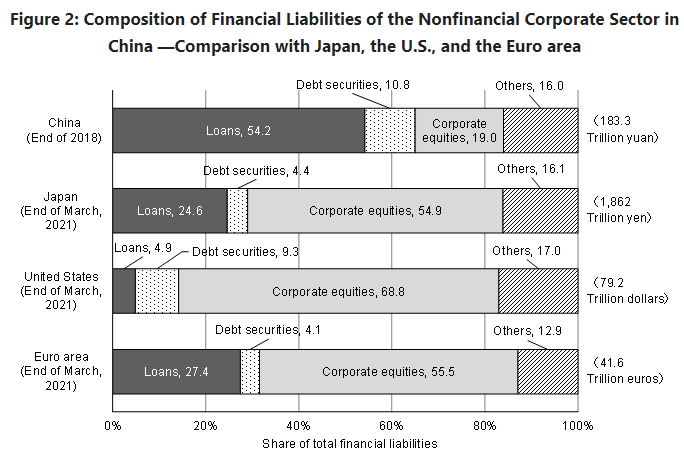

This is not to say that the Chinese won’t act to prevent an unruly market. The last time they did was following a sharp sell off in 2015, which was in response to a speculative rally in 2014. This time around the speculation is more likely on the short side and is thus why they appear to have acted. But this is not about ‘pulling in overseas investment’, it’s a long time since China needed external capital and indeed, most Chinese corporates fund cap-ex through cash flow and private credit. We can see this from the second graphic from the same source.

Source: Research Institute of Economy Trade and Industry , Japan.

The China market sell off has been more about international liquidity than fundamentals

It’s been international liquidity flows that have been important for China, (as they have been historically for Japan) as many international investors are increasingly splitting China out from their overall EM baskets (and selling down). This should be good for areas like Taiwan and Korea on a simple flow basis, but also on a quality and cash flow view point. So too Japan, which continues to attract attention as it wakes from its 30 year self induced coma, benefiting from a combination of value, some positive operational gearing and growth in tech and robotics in particular and also in the wholesale and trading conglomerates.

(At this point we should remind readers that this is not financial advice, it is for information purposes only. Please do your own research and talk to your financial advisor)

Medium Term Risks

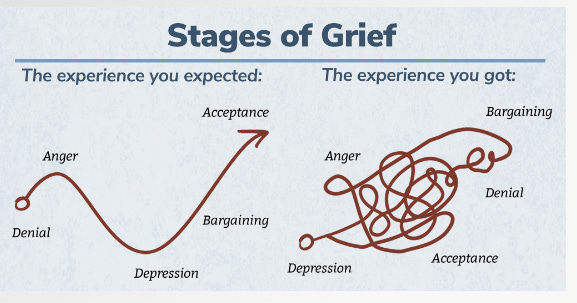

The continued positive polling for Robert Kennedy Jnr looks to be a key risk for the Democrats, threatening to split the Democrat (in effect Anti Trump) vote in the manner of Ross Perot, whose 18% delivered the White House to Bill Clinton. After a long period of ‘denial’ that Trump could come back, the media and the markets are now being forced to consider what it might mean.

However, unlike the classic Kubler-Ross cycle of five stages of Grief, the media in particular have been crashing about through all five stages recently - as illustrated by this schematic.

Source Cruse Bereavement support

The Anti Trump Media (i.e. almost all of them) had been in denial about a second Trump term, boosting all or any of his potential opponents and relishing the prospect that somehow the ‘legal system’ would prevent him running, including certain Democrat states banning him having his name on the Ballot. But with the last remaining ‘forlorn hope’ of the Democrat Donors to the Republican Party, Nikkei Haley, coming second to ‘none of the above’ in the Nevada Primary, it looks like he is back. And with Joe Biden not even taking the 3 minute softball interview at the Superbowl they are bouncing around all over Kubler-Ross. Interesting to note that the betting markets now seem to be pushing for Michelle Obama to ‘step in’ and replace the crumbling Joe Biden rather than previous favourite Gavin Newsome.

Trump’s likely policies could be very good for Europe

Trump then is probably the biggest medium term risk/uncertainty for markets. Perhaps ironically, given that the EU is dominated by the very Globalists that despise Trump, his pre-announced policies might do the EU a big favour. We know for example that Trump has said he will act at the Border and also that he will ‘Drill Baby, Drill’ for oil, (see previous post Oil and the T word) both of which chime with the Anti-Globalist rhetoric being expressed across Europe in the farmer’s protests. While (inevitably) being portrayed by the (pro Globalist) establishment as ‘far right’, these populist protests are likely to have an impact at the national level and also at the June EU Elections, (see Farmers at the Gates) with implications for the Green Industrial Complex, as well as those Global Companies currently benefitting from private sector monopolies seen as secured by lobbying and which would make good politics to revoke. Trump meanwhile has also said he will get rid of DEI policies and has previously questioned the role of NATO and the massive US expenditure on overseas military bases as well as saying he would end the war in Ukraine.

We would suggest that it is the prospect of a cease fire in Ukraine and populist pressure to cut Russia tariffs that is driving the sudden rachet-up in bellicosity this year. The ‘Defense’ Industry needs something to (expensively) defend us against and being in some form of war makes it difficult to cut Budgets.

Long Term Trends

We have discussed how in a savings driven economy, lower interest rates tend to mean less spending, rather than more spending driven by more borrowing. In other words, the US-centric economic models on interest rates and spending have tended to work in reverse in countries like Japan and much of Asia. As such we see a normalisation of interest rates shifting the spending patterns away from leveraged balance sheets to savings rich balance sheets with income and cash flow. The higher wages and higher return on savings in Japan for example are starting to drive consumption.

The other factor is confidence and risk taking. Post Covid, western consumers dashed out spending (helped by large government handouts and having been unable to spend for 2 years) but the Asian and particularly Chinese Consumers have taken the attitude that ‘it might happen again’ and are still deleveraging balance sheets.

But to return to our Assets and liability tables above, the long term trend in China is undoubtedly to try and build out the pension/insurance policy part (termed insurance pension and standardised guarantees in the graphic) to the 30% or so level seen elsewhere. And we may find that, far from trying to prop the market up, the ‘National Team’ are buying up corporate equities as the basis of a long term pension system. After all, every time they ‘shock’ western investors its because they are taking a long term investor view rather than a short term trader one.