After a strong March and a solid first quarter for equity markets, risks are edging up again and, as always, they are coming from the Fixed Income markets. Following a lacklustre first quarter, where the US 10 year bond yield drifted up towards the top of its 4-4.5% trading range, the latest US ‘inflation print’ has got the bond traders panicking and the market expectations of a Fed rate cut receding rapidly, with the fixed income mood further depressed by a badly received Treasury Auction that left yields above that psychological 4.5% level. With a new tax year bringing an unwelcome Capital Gains Tax bill for retail investors on (welcome) capital gains, momentum seems to be fading in momentum stocks and we may see the equity market mood shift to profit taking, especially in these areas.

Short Term Uncertainties - tax, bonds and the Fed

Even before the latest CPI inspired selloff, US bonds had been drifting lower, with the US long Bond ETF – TLT – having now completed a full 50% reversal of its rally from the October lows and essentially bonds remain in a bear market. By contrast, an equity bull market has been developing from the oversold rally that began in q4 2023 (our view has been that the bear market ended in early 2023, but that it might take time for a new bull market to emerge). March saw a good performance in equities across the board, reflecting a welcome and continuing broadening of returns, as investors sought to diversify away from US Tech, leading to a solid first quarter return and establishing a bull trend within our Model Portfolios across most equity themes, countries and factors.

However, we suspect that a new tax year (and some Capital Gains Tax bills) is likely to put something of a dampener on things short term and likely take some liquidity out of markets. As such, we notice that there is already a modest correction underway in the momentum factor (the biggest factor winner year to date). Also that our ‘pair chart’ of XLE (Energy) versus XLK (Tech) has corrected 9% year to date in favour of energy, and 16% from the January peak as Tech (which dominates the momentum factor at the moment) starts to fade.

In our model portfolios we have moved back to neutral in some of the better performing areas like Robotics and Fintech, as well as Digital security and Japan as the risk/reward looked a little skewed. We have also been watching China Tech closely for some time and believe that here the risk reward has improved.

We believe that the political interference in the already noisy high frequency data driven markets (see Gold and Goldilocks) is going to add even more uncertainty than usual and likely drive bond volatility - and by extension also likely equity volatility - higher. And the MOVE index of bond volatility is something that keeps both Jerome Powell and his predecessor Janet Yellen, now at the Treasury awake at night.

Bond Volatility is what keeps present and former Fed Governors awake at night. And it’s starting to rise.

The biggest short term risk is thus likely to be from the bond markets. Not only have the economic bears/bond bulls been revising their opinions on the need for the Fed to Pivot, but there is also ongoing concern about supply, as the House passed another highly expansionary Budget. The problem increasingly is that the buyers of US Treasuries are no longer price insensitive Central Banks, but price sensitive domestic buyers and importantly financial institutions facing mark-to-market ‘risk’. In 2019, around half of US Treasury issuance was taken up by overseas investors, now it is more like a third and with the Fed stepping back it is ‘other domestic lenders’ that are setting the price.

The concern is that they can generate negative feedback loops as we saw last March with the US regional Banks, notably SVB, where mark-to-market bond losses require more capital, which can only be met by selling more bonds. In turn bond volatility spikes, triggering selling of the (now) more volatile asset by risk parity funds and so on. This was not dissimilar to the issues faced by UK pension funds the previous September.

Last March, the MOVE index of bond volatility spiked sharply higher, as it did to a lesser extent in September 2023 and in September 2022. None of these occasions were good for Equity Markets.

Having recovered from the Regional Bank/Bond sell off at the end of q1 2023, equities rallied, only to be hit in late July by another bond driven shock - this time we believe from Japan (as we wrote about in a note Japan has woken and thinks are going to get broken). The problem here is that while foreigners may be participating less in the flow, they are still a large part of the stock of US Treasuries and if they are forced to sell into a market where the Treasury are also selling, then things can get ugly.

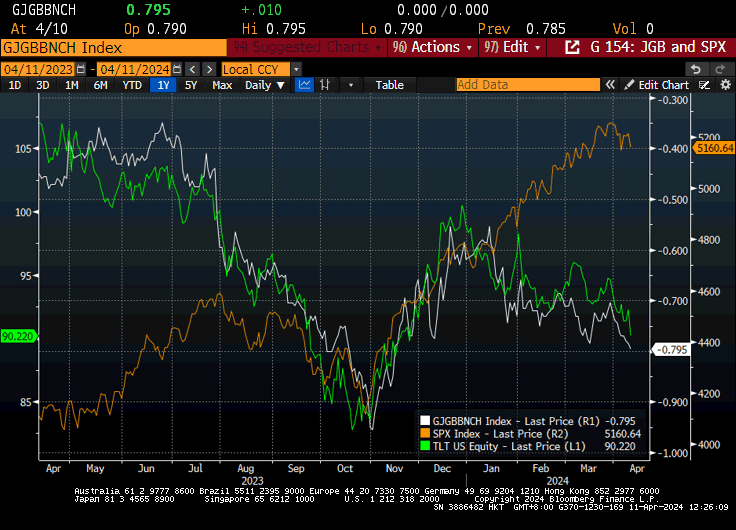

With the end of Zero Interest Rate Policy (ZIRP) and the Japanese economy waking from a self induced 30 year coma, the Japanese government bond yield started to rise last year- as shown (inverted) in the chart - causing mark to market losses for holders of JGBs like the Japanese life companies. In a classic case of the old market dictum that in distress you sell what you can, not what you want to, they sold off US Treasury holdings and Gold - both of which had done very well in Yen terms and thus didn’t necessarily require booking a loss. However, to add another layer of complexity, the fact that these bond holdings were usually hedged back into Yen meant that selling them involved closing out short $ positions and hence a sell off in the Yen.

JGB Panic dragged markets around

As the chart shows, the US Long Bond and the JGB market moved in tandem in 2023 and the recovery from the distressed selling of JGBs in Q3 2023 coincided with not only the powerful Q4 rally in bonds, but also in the US Equity market.

The fact that bonds have gone down while equities have continued to rally is not necessarily to infer that equities need to follow bonds down, although discounted cash flow models are obviously going to be giving stretched valuations, more to say that any sharp rate of change in Bonds associated with mark to market losses risks triggering similar feedback loops. Hence the Fed (and equity investors) need to keep a close eye on things like the MOVE index of bond volatility as well as on JGB yields and indeed the Yen.

As well as causing bond yields to drift higher, the delay in/lack of cuts in rates has meant continued flows into US cash products and thus the US$ has remained relatively strong. Gold, which appears to have replaced bonds as the ‘risk off’ asset of choice, finally broke out of its long term consolidation pattern at the beginning of March, catching many by surprise. Meanwhile Oil and other commodities have also flipped the traditional inverse correlation with the $ and have been rising, further pushing consensus back towards a more inflationary stance.

Within Equities, the US remains the largest (over 70% of Global Market Cap) and the most expensive of the major markets and much of the recent activity in our Model Portfolios appears to reflect diversification away from US tech stocks. European Banks in particular had a good month in March – jumping over almost 14%, as the underlying story on dividends and buybacks became more obvious during the reporting season. Meanwhile, some of the strongest returns year to date have come from Asia, notably Japan, then Taiwan, but these have moved into a consolidation phase since the mid-march options expiry, suggesting a lack of follow through buying, likely around not only quarter end but also financial year end – traditionally this was always important in Japan. Early April has seen some small profit taking across the board after a strong first quarter and a fading of momentum in some of the big momentum stocks like Nvidia.

Medium Term Risks - Politics, commodities, and Japan

While the noise traders obsess over US jobs numbers and the inflation data as well as dot plots from the Fed now apparently telling them that the Fed won’t ease, we think that they most likely still will, because actually the Fed were always going to raise rates past the natural rate (c4.5%) to allow a modest adjustment back. However, they were never going to take them back to 2% as many bond bulls were predicting. As such we see this as a reality check for macro traders and bond bulls rather than any new fundamentals. Also, as noted above Politics means that the glass on US macro is going to be flip flopping from half empty to half full for the rest of the year, with the bond markets and rate expectations following along.

Political spin is going to distort the already noisy fixed income markets

The prospect of a new US President is close enough to be a short term uncertainty, but as a medium term risk the key questions are nonetheless around energy policy (Trump plans to drill baby drill) and, of course, foreign policy. A solution to Ukraine and an ending of sanctions would be transformative for the EU economy - especially Germany - although we would caution that the strong performance in European Value stocks in March was largely down to European Banks and some autos, where the demand is more global.

Indeed, the irony is that one of the key drivers for concerns over US inflation is coming from commodity input prices, and they are almost nothing to do with US demand or interest rates - they reflect supply shortages and global rather than US demand. As such, raising rates in the US would have little impact (not that Central Bankers necessarily think this way). Whether the recent strength of commodities is a medium term trend, or just short term speculative flows is unclear at the moment. Certainly if we look at the chart from our friends at Redburn Atlantic, Copper’s recent rally doesn’t seem to be confirmed (yet) by the historically correlated but more industrial indicators such as Chinese steel and the biggest moves in mining stocks have been in the ones digging out the precious metals rather than the industrial ones.

Chinese Steel not yet agreeing with Dr Copper

Source Redburn Atlantic

In fact, we think that the bigger medium term risks for equities also comes from Bond markets as a result of supply – more specifically the Federal Budget which continues to explode despite the giant increase in debt due to Covid. Funding this is an increasing challenge and the Fed can/will only monetise it for so long.

We noted (a Bold view on bitcoin and gold ) that the US Banks have asked for a permanent extension to the capital requirements that would allow them to effectively run a carry trade into US debt from deposits. While this would help the Treasury and no doubt bank profits, it would also imply lots of duration risk (remember Silicon Valley Bank). The Fed, whose job is really to maintain financial stability, is thus likely to be keeping some powder dry to ensure that there isn’t an accident in the bond markets – thus rates will be kept high enough to provide confidence on inflation, with the prospect of modest easing to offer a capital return, but some easing will be ‘saved’ in order to combat any sudden sell-off similar to q3 last year.

US monetary policy is being driven by both the Fed and the Treasury and will be structured to maintain stability in bond markets

This request for ‘bank QE’ coincided with the March spike in Gold, which along with Bitcoin are something of a canary in the coalmine warning about currency debasement. However, while the medium term short dollar story remains very important, we think it is best played through diversification for now. We still see the sense in diversifying from the US$ and US$ tech and see value in the Japan wholesale trade, European Financials and EM ex China. Also global quality and Quality Dividends. We see the fixed income markets as having become more sanguine on the economy and thus by extension less excited about a dramatic cut in rates, but are wary that the growth in the US is sustainable; in effect it mainly comes from increased borrowing and spending, which is by definition more inflationary.

China has been much more of a value trade so far this year and had a strong February/March. However, it has run into some profit taking and we await clearer evidence that it has complete the process of moving from weak hands to strong hands. While we are not quite ‘there’ yet, we believe that the process is almost complete and for those taking a 12 month view the disconnect between the consensus macro view and the reality is large enough to make a compelling case.