On 17th March 2000, a bolt of lightning knocked out a cooling fan and caused a small fire in a Phillips chip plant in Albuquerque and exposed the problem of single company sourcing for two of the biggest companies in the world at the time, Nokia and Ericsson. Nokia reacted quickly and secured a new diversified supply of the chips required, while Ericsson sat it out, with pretty disastrous consequences for profits and its share price. However, while the relative behaviour is cited as a textbook study of supply chain management, within six months, and following a profit warning from Ericsson in July, both stocks had fallen by 40% and while Nokia had a rally in q4, within 2 years, Nokia was down 75% and Ericsson an astonishing 96%.

Of course we know this was against the background of the Dot Com crash, but in many ways it was a function of impossible expectations on future profits and the amount investors were willing to pay for them. At their respective peaks, according to Bloomberg data, Nokia was trading on 15x sales, while Ericsson was on 8.3x sales. Within a year that had dropped to 2x and 0.9x respectively - at one point Ericsson went as low as 0.15x. Incidentally, both are currently on around 0.6x.

Thanks for reading Mark’s Substack! Subscribe for free to receive new posts and support my work.

The Crazy logic of 10x Sales

At this point it is worth recalling the words of Scott McNealy, the boss of Sun Microsystems, back in 2002. Here I am lifting wholesale from a recent piece (Party like it’s 1999) by my good friend Mr Louis Gave - since it’s a quote I am sure he won’t mind.

“Two years ago we were selling at 10 times revenues when we were at US$64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at US$64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Scott McNealy, CEO Sun Microsystems, 2002

(hat tip to Louis Gave)

We are not sure what John Chambers, thought when his company, Cisco, was trading at 44x sales, but the logic applies the same way. Of course there was growth, but as we saw back with the so called Nifty Fifty stocks in the late 1960s (see Jeremy Siegel, Stocks for the Long Run), even though the earnings did come through, the multiples paid for those earnings collapsed. For context, by 2002, Cisco had dropped below $10 and more than 20 years later is still only at $48 and 3.5x sales.

The perils of Vendor Financing

Another issue that came back to bite the Nokia and Ericsson and their investors was the issue of vendor financing. With the European governments having taken around $128billion of the Telecom companies’ cap ex in the form of licenses, leaving them turning to their equipment suppliers for vendor financing. For example, in 2001, Nokia agreed to lend Orange Eu 2bn to fund Eu 1.5bn of its products, it also lent Hutchinson Whampoa $650m to buy its products. This inflated their sales in 2000/2001, but then saw a rapid reversal as the credit lines were run down. Vodafone, which had an average Price/Sales of 11x in 2000, with a peak at 16x, was equally involved in the process. Like Nokia and Ericsson, it too now trades on a Price/Sales of 0.6x

The Dangers of Indexation

At the peak of the market in 2000, Nokia was the largest stock by market cap in Europe and Vodafone the largest by far in the UK. At the time, both required sleight of hand by managers to get around the 10% maximum holding under Unit Trust rules, while in the US, although Cisco had risen 1,300 % in three years to become the biggest stock in the market it was ‘only’ 4% of the S&P.

So why bring this up now? Well, and at this point we should obviously point out that none of this should be considered investment advice. It is for information and hopefully entertainment purposes only. Please do your own research and contact your financial advisor. The answer is pretty obvious, we have a number of stocks that demonstrate all of the above characteristics in that they are

- concentrated in their supply chain

- Trading on very high multiples of current sales

- Have a dominant market share assumed to remain unchallenged

- Selling their products to connected parties

- Are a ‘must have’ on the basis that they are a key part of a benchmark for passive investors whose risk management is simply against an index.

Most obviously there is Nvidia, the current market darling dividing the winners and losers in the S&P 500. It is currently 4% of the Index, behind Apple and Microsoft, trades on 40x sales and makes 70% of its revenue overseas, 20% in China, 20% in Taiwan and 15% in Singapore (possibly also really a route to China). More importantly of course is that it makes everything in Taiwan, where there is a risk of something rather more serious than a lightning strike. Admittedly a small one, but in a world that is putting Chinese stocks on 1x sales based apparently on the same risk, there seems to be a disconnect.

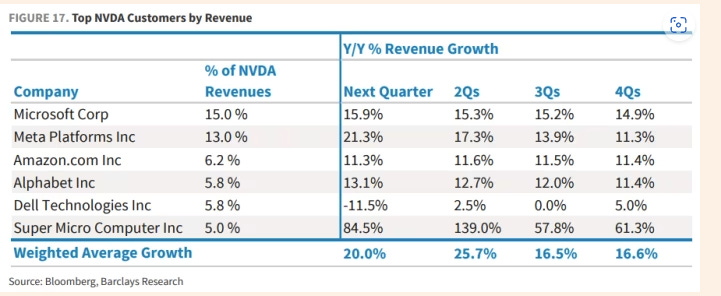

Currently, Nvida has a 98% share of the Data Centre GPU market, but almost a third (28%) of its sales here are to Microsoft and Meta and, as the table below from Barclays Credit analysts point out, half of its sales are derived from only five companies.

The problem is that its tech customers are also its competitors, all looking to build their own chips. This is not to say they will do so straight away, but rather that the problem with a 40x sales multiple is that you are vulnerable to any hiccough in forward earnings - as Ericsson found.

The perhaps a more intriguing issue is that Nvidia’s 7th largest customer according to Barclay’s research was a company called Coreweave, which purchased 40,000 of the H100 GPUs at $150k each. Nothing wrong with that, except that Coreweave is a startup at least partly funded by Nvidia itself, which rings alarm bells for those of us that remember the trouble that Ericsson got into in back in 2001.

What else might be happening?

Passive ETF indexers being front run (again)? Or Tech as the new Bonds?

Last year we noted that before the popular momentum ETF was adjusted away from Energy to Tech in its bi-annual rebalancing, traders were selling energy stocks and buying tech and suggested that this may well have contributed to the move up in Magnificent 7 stocks ahead of time. This year, looking at the popular SPDR Technology ETF, (XLK US) we notice that currently it is weighted 23% Microsoft, 19.7% Apple and 6.3% Nvidia and is reweighted quarterly. By contrast, the percentages in the monthly rebalanced SPY ETF tracking the S&P500 are 7.14%, 6.33% and 4.26% respectively. In effect, Nvidia is currently half the weight relative to the other two in the Tech ETF that it is in the SPY. We believe that this could that be behind some of the momentum buying.

Equally, it appears that the large US Tech stocks are having a divorce from fundamentals in the same way that the bond markets did under QE - fundamentals don’t matter. Only flow does. An 80:20 barbell of Cash and Tech stocks (or even better call options) would be an interesting strategy right now. Perhaps with a mix of a Bitcoin ETF. That’s probably what the AI traders powered by Nvidia’s chips are doing!

Conclusion.

With the caveat that selling stocks short into a momentum rally is always dangerous, there are sufficient alarm bells around this AI hype to warrant a reminder of times past and certainly to caution participation for anyone other than active traders. (reminder, not investment advice). When investors wanted to buy the ‘picks and shovels’ of the internet boom back in 2000, we saw similar rapid price movements. However, as noted it only took a small fire in Texas to trigger a chain of events that led to a profit warning and a collapse in the magical thinking propping up the share price of two of the biggest market cap stocks in Europe, which then extended to the wider sector.

The problem was the implied parabolic earnings required to justify double digit sales multiples and the associated passive/closet indexing that was substituting index tracking for risk management. Currently the magical thinking on AI is such that everything has to ‘go right’. Investors are selling China on the (very small) chance that China invades Taiwan, for example, while seemingly ignoring that such a move would send these stocks on double digit sales multiples down 90%. They are also assuming that the biggest customers will remain captured, that there is no emergent competition and that, even without an invasion there is no disruption from tariffs into their biggest end user market.

A barbell where everything is expected to go wrong for most of the market but everything is required to go right for a small part with a strong narrative might work for an active trader, but doesn’t make sense for a long term investor. The risk manager stuck in the middle trying not to underperform a benchmark probably has to hold their nose and join in. But we would be happy to sit this one out.