For a recording of this article, go to our new podcast and listen here

July generally sees favourable seasonality, albeit with lower volumes and liquidity. It is also often seen as ‘a half time break’ , an opportunity for looking back over the last six months and ahead to year end. This year the main themes are seemingly around the path of interest rates and the extreme narrowness of the equity market rally, which has been all about Mega Cap tech, something we see as being mainly about market mechanics, but which has been wrapped in a new narrative around AI. Meanwhile, we see Geo-politics slipping down the agenda, positioned now as a ‘known unknown’ as well as a reduction in some of the more extreme economic bearishness that prevailed back in January. As is often the case, investors’ perceptions of the economy reflect their recent experience in markets.

Looking forward, we expect the broader outline of ‘the new New Normal’ to continue to emerge with the end of dis-inflation and thus inflation itself settling into a new 2-4% band. Short rates will trend towards a ‘normal’ level of 0% in real terms (so 200bp higher than the previous range) with modestly upward sloping yield curves offering term premium. In other words, everything, inflation, cash and bond yields is shifting to a new regime some 200bps higher. Equities, having already made the discount rate adjustment last year, will move to be about cash flow and earnings rather than multiple expansion and contraction, while commodities will remain as much about supply as demand. In FX we see an unstoppable geo-political trend of a multi-polar system evolving with two currency trading blocs of The West - still centred around the $- and The Rest - much more bi-lateral but increasingly centred more around the Rmb. This is not about the end of the $ as a Reserve Currency, it is about a significant reduction in the size of the $ banking system.

To achieve all this, we need an end to policy errors. Here’s hoping.

The macro is largely conforming to the new ‘new normal’ playbook

We began the year broadly in agreement with the consensus view that both inflation and economic activity would be slower, but were sceptical of the follow-through idea that this would necessarily mean a further leg down in equity markets. In our view, while the first leg was due to tighter monetary policy and discount rates moving sharply higher, the second leg of a bear market would require that earnings started falling. We were doubtful this was going to happen and this has so far proved to be correct. While we are not yet ready to call this a new bull market, at now over 250 days it is difficult to argue that this is just a bear market rally. It is however, largely consistent with our view of a new ‘new normal’, where normal companies can make normal profits and good companies can make good profits. This is an environment where interest rates are ‘normal’ in balancing out borrowers and savers and sound balance sheets and positive cash flows rather than financial engineering are the key drivers of returns. Looking forward, earnings are key, both to sustaining the rally and to which stocks to own within it.

Within equities, the first half has been all about the Magnificent Seven Mega Cap tech stocks, with AI as the new narrative

The H1 Equity rally itself has been highly unusual however, in that, until the end of May, while 493 of the S&P500 were essentially flat year to date, ‘The Magnificent Seven’ mega cap tech stocks were all up over 50%. To a large extent this was simply an unwind of the sell-off in q3 last year, on the old premise that something that goes down 30% has to rally 50% just to get back to where it started, but it has nevertheless represented a serious challenge for active managers, very few of whom would have been in line, let alone overweight the very largest stocks in the market. By contrast, this is exactly where the short term momentum traders will have been. The index trackers meanwhile will have, by definition, been in line. Thus, after a year when most investors, passive and active went down in line with the market, this year many of the active ones have failed to follow it back up, doubtless making for some awkward conversations.

Note however, that both the equal weighted S&P 500 index and the market cap weighted S&P500 index are down about the same (still some 8% below) compared to where they were in December 2021.

Remember, it takes a 50% rally to recover a 33% loss

Bonds meanwhile appear to have moved into a new range for the US 10 year, from one centred around 1.5%, to one now centred around 3.5%, consistent with a shift in the inflation regime from a band of 0-2% to one of 2-4%. There appears to be some evidence of asset allocator and long term investors bond buying at around the 4% level, ‘locking in’ some expected real yield for asset/liability managers, although the short term traders continue to focus on the high frequency data and the ‘pause or pivot - or (now) go higher? debate. From our perspective, with the Fed having finally ‘paused’ in June, we see something close to a peak, before slowly adjusting back to something closer to zero % in real terms. The speed at which this occurs will be key in forming perceptions of re-investment risk for bond managers - locking in the higher rates at the short end now might look attractive, but on a five or ten year horizon the risk is that when that two year rate rolls off, the new rate might be considerably lower. When, then, to move duration?

An end to policy errors

The biggest risk around a new New Normal of course is that it at least partially assumes an end to the recent run of policy errors. Over a decade of Zero Interest Rate Policy (ZIRP) had not only failed to produce the desired high street inflation, but had instead produced the exact opposite, high street dis-inflation, through the fact that the stimulus to supply produced by a low cost of capital far outweighed any stimulus to demand from increased consumer borrowing, something the modelling failed to pick up. Nor did it appear to learn from the real-life Japanese experience that in a savings rather than a borrowing economy, or when consumers are deleveraging, lower rates are more likely to increase savings than consumption, in the same way they create pension fund deficits.

Meanwhile, the artificially low cost of capital had produced an asset price boom/bubble that was not only entirely consistent with previous economic history but seemingly also entirely ignored by the central bankers. For, as we have said before, it was the Zero Covid policy that managed to simultaneously restrict supply by collapsing the global supply chain and stimulate demand through massive money printing going straight to consumers and thus create the inflation we now see. Again, pretty textbook stuff, but seemingly a surprise to policy makers who are still talking about non-farm payrolls and wage price spirals. The risk therefore is that they make the same mistake, but in a different direction and collapse both demand and supply. Certainly, the bond vigilantes are egging them on with talk about ‘credibility’ and hyping up the short term data as if every ‘print’ on payrolls, CPI, PPI that comes in higher than ‘forecast’ needs to be met with another round of interest rate increases. We have to hope that they are ignored.

The biggest macro risk is that Central Banker repeat their mistake on interest rate policy - only in the other direction. Low rates didn’t cause inflation and high rates won’t stop it, but they will put pressure on many areas of the economy

In the meantime, this dramatic regime change from QE and Zero Interest Rate Policy is having clear re-distribution effects in the real economy away from borrowers and towards savers, as well as within savings markets themselves, as Money Market Funds attract huge inflows at the expense of other asset classes, exaggerating the problems of liquidity in many of them. After more than a decade of mis-priced capital, many corporates and consumers now have fragile balance sheets and we are far from certain that the Central Banker’s fancy computer models - which after all completely failed to predict the actual impact of QE - allow for any of this. Cash is king as they used to say, but the reality is that risk free returns on cash are now actually too high for savers, while the cost of capital is now too high for borrowers. This needs to be temporary.

From mean reversion to momentum and risk aversion.

For long term investors, markets in H1 neatly captured the behaviour of the other two of the three tribes in Market Thinking, during a period that we would characterise as Mean Reversal meets Momentum and Risk Aversion.

During 2022, everything went down except the $ and in Q1 2023, everything flipped the other way, in a form of mean reversion led by the very traders who had been aggressively selling during the previous year. This covering of short positions was most intense in the mega cap tech stocks and led to NASDAQ sharply out-performing the S&P going into Q2. This move was sufficiently large to cascade down to the medium term asset allocators who scrambled to go long NASDAQ futures against S&P500, in doing so adding Risk aversion into the mix and triggering a further round of momentum buying by traders - now including retail. As we noted in an earlier post, one phenomenon that needs to be watched is the composition of the US and Global Momentum benchmarks and the ETFs that track them. Because they rebalance only every six months, there appears to be a rebalancing trade ahead of time; this latest June rebalancing saw energy collapse as a weighting while tech jumped, in our view helping explain a good deal of the April/May price behaviour.

Traders covered shorts and asset allocators bought NASDAQ to ‘reduce risk’, leaving long term investors struggling as to whether to join in or sit it out

Many long-term investors have ‘missed out’ on this rally of course and are wondering whether or not they should join in and there is certainly a feeling of FOMO, albeit it weighed against muscle memory of NASDAQ H2 1999 - the last time that the Tech stocks were this ‘hot’ relative to everywhere else. In our view we are more likely to see another mean reversion rather than another momentum/risk aversion combination so would be reluctant to chase it, while not seeing fundamentals as challenging as 1999. Indeed, the encouraging thing is that history shows a narrow rally more often leads to catch up of the under-performers rather than the whole market collapsing.

Looking into H2 we feel that the noise from momentum and mean reversal will die down, leaving more room for fundamentals and the longer-term investor perspective to hold sway. This points us back to sound balance sheets and positive cash flow, the essential attributes for surviving the ‘new’ New Normal.

Short Term Uncertainties

The strong first half has certainly revived animal spirits - in the US at least - and with the summer holidays approaching we expect to see this continue, although with thinner volumes and more volatility it’s not going to be plain sailing. The US investor has flipped from all time bearish at the start of the year, to almost 2021 levels of bullishness, which ironically is something of a risk signal, the AAII Bulls versus bears chart is often seen as a reverse indicator and here we are right back up again - especially in the last month.

A bit too Bullish?

This over-confidence is probably the biggest short term risk to markets - options traders have left the VIX at very low levels again and the current technical structure is such that any spike in implied volatility (which we like to think of as the price of put options) will trigger selling from the risk parity community. Also, as far as the US is concerned, the majority of companies are in closed season for buybacks at the moment, removing a ‘buyer’ in the event of any dip to be bought.

The other main concern is how far the NASDAQ stocks can rally without a meaningful correction and whether that means a rotation back into equal weighted S&P or a broader sell-off. On balance we think the former, but in thin markets it could certainly unwind a lot of the gains year to date, such that active managers who have been the right side of the trade may well be tempted to take some profits before heading to the beach.

Elsewhere, the bond traders, having previously convinced themselves that the Fed would ‘pivot’ and cut, are now of the view that the Fed will set policy in line with their (the markets) beloved non-farm payrolls - something it has never actually done in decades - albeit consistent with some of the more hawkish Fed policy makers. As such, we would expect some heightened ‘uncertainty’ about the exact peak, with markets flip flopping between hiking or cutting on every high frequency data point - as well of course as attributing huge importance to Fed meetings and utterances. To the extent that the strong bounce in equities is feeding a positive economic outlook, the bond markets need to push a negative economic outlook of inflation needing ‘even tougher’ Fed policy. This narrative fight will likely be a feature of Q3

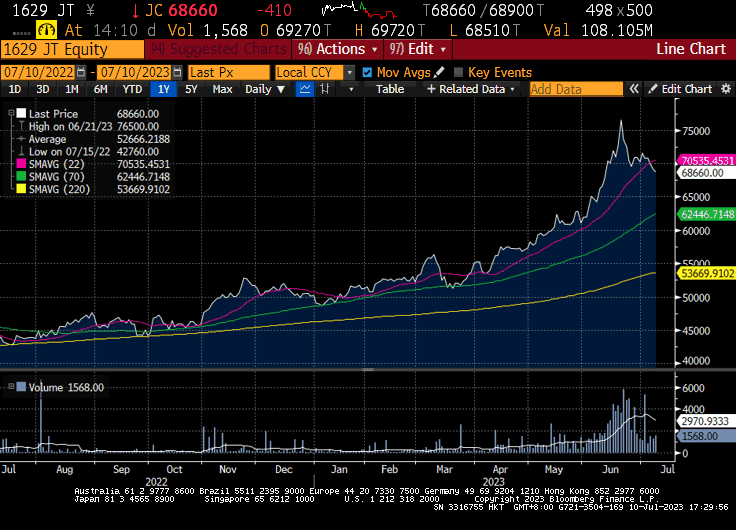

One other point on the Yen is that it looks like recently it was being used as a funding currency by traders (the $ was too expensive) so that we need to watch this as a risk indicator - right now saying risk coming off. We are closely watching the Japanese trading companies for example - the so called Warren Buffet trade of borrowing in Yen to run a ‘carry’ into 3.5% yielding economically exposed stocks has been a great performer over the last 12 months, but especially in q2. Looking at the volumes in the chart below - concentrated in June - as well as a 50% retracement of the June spike and we get a picture of a strong long term trade being taken over by leveraged traders in the short term.

Froth blowing off the Japanese trading companies?

Medium Term Risks

Aside from the question of whether to chase the mega cap tech stocks, one of the other big questions for long term investors is what to do about China? While the Chinese economy has now fully opened up, the stock market has seen headwinds rather than tailwinds, leaving the Shanghai Composite index for instance flat year to date and broadly unchanged over 3 years. For many, the real issue is that it is over 30% lower than the late 2020 highs and the market as represented by the more mixed tech and traditional Shanghai Shenzhen CSI 300 index continues to demonstrate bear market conditions of selling the rallies rather than buying the dips.

China still seeing stocks transition from weak hands to strong hands

We see this as having started with the dramatic sell-off in the China Education stocks in August 2021, when Xi’s declarations on Common Prosperity effectively called time on the notion of China as the world’s largest emerging market for western investors. It also called time on the magical thinking behind the ADR market (that they were simultaneously 100% foreign owned and 100% Chinese owned) which triggered an ongoing process of these stocks moving from weak hands to strong hands. It is also undoubtedly connected with Geo-Politics and the perceived risk that the US and other western authorities will effectively extend their sanctions regime into investment holdings. As previously discussed, the ESG infrastructure allows lobbyists and external actors to effectively determine the scope of private investment portfolios and there is no reason why that can’t be utilised for foreign policy ends. As well of course as old fashioned protectionism. Lobbying Congress to seek to ban your competitors on ESG or National Security grounds is increasingly common, although it can backfire - as US companies reliant on imports of strategic minerals from China are realising.

In order to justify this dis-investment, it is being backed up with a narrative about how ‘weak’ the Chinese economy is - something that also suits the Geo-Political agenda. This is of course despite the fact that the Chinese economy is predicted to grow by over 5% next year while the US and Europe are barely 1% or less. It is thus important to separate out the price behaviour (effectively forced selling) from the new ‘China bad and also weak’ narrative. The Chinese economy continues to evolve, it no longer ‘needs’ the west to buy its exports - albeit they are at record levels - and while the infrastructure demands remain as high as ever, the restructuring of the property sector balance sheets is an entirely different issue from demand for (and supply of) housing. Inflation remains low, interest rates were not set at the ‘wrong level’ for a decade and the energy policy is coherent.

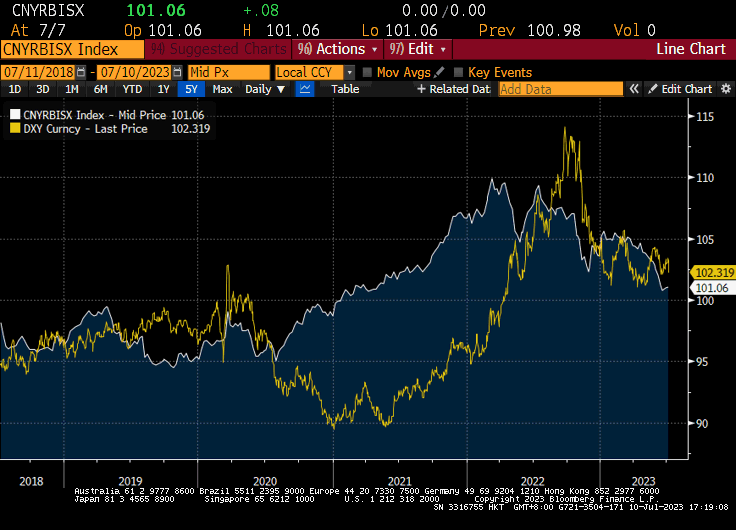

One point that has been somewhat overlooked in recent weeks , is that the Chinese appear to have put in a sneak depreciation of the currency.

In the meantime, it is interesting to note that not only has the Rmb been allowed to depreciate against the $ in recent weeks, but it has also depreciated against its trade weighted currency basket, a more important measure of its competitiveness, seemingly targeting the Yen, whose recent weakness against the $ appears to reflect the macro traders’ flip from the Fed cutting to now raising rates. Note however, that over the last 5 years the Rmb basket has ultimately not ended up that different than the US$ basket, and particularly since mid 2022 when the Fed started tightening.

China becoming more competitive against other exporters

Long Term trends

The surge in the mega cap tech stocks has similarly been supported by a narrative, this time it is AI, and these companies are seen as selling the picks and shovels for this new industrial revolution. While we do agree that this is a proper ‘next leg’ for productivity - this time in the service sector - we are a little wary of the idea that it will be all the biggest tech companies that will win. After all, if we are to take the internet as our precedent, almost none of these companies existed 20 years ago and buying Cisco and IBM as ‘winners of the internet’ would not have been a sensible strategy. The challenge remains to identify the next Apple, Amazon, Meta and Nvidia. One area we are looking at from a thematic point of view is Cyber security; obviously the more AI is driving things on the one hand, the more important security is on the other. Moreover, with Google just announcing a breakthrough in Quantum computing, it is only a matter of time before all the encryption algorithms need resetting. Not actually difficult, but now necessary.

Bottom Line - narratives shifting

The narrative about inflation and growth is shifting, despite the noise in Bond markets, to one of lower growth and lower inflation, while the narrative on equities is also shifting - away from the second leg of a bear market, to, in some cases a new bull market. We never really believed in the former and equally are reluctant to commit to the latter. Instead, we would focus on quality, strong balance sheets and positive cash flows. The narrative on China we regard as self serving, to justify politically influenced selling, something we expect to fade (and thus the narrative reverse) over the next 12 months. The narrative on AI meanwhile, has been conjured up to justify the buying of the mega cap tech stocks, but we do not feel it is robust enough at this point, certainly not to be an investable theme in its own right and certainly not really robust enough to justify the valuations in these ‘picks and shovels’ companies.